A Silver Lining in Brazil

The USDBRL recently broke above a descending channel, signaling further BRL weakness; an unusual occurrence given the ongoing shift to easing cycles by major global central banks.

On September 18th, the Federal Reserve (Fed) cut rates by 50 basis points, marking its first reduction since the pandemic. Several other central banks, such as Bank of Canada (BOC), European Central Bank (ECB), have continued their ongoing rate cut cycle in the past few months. While uncertainties remain about the pace and extent of these cuts, there is a clear consensus among major central banks to adopt a dovish stance.

Historically, monetary decisions by major central banks, especially the U.S. Federal Reserve (Fed), have directly influenced the USDBRL exchange rate. Higher U.S. rates attract capital inflows, strengthening the USD and weakening the BRL. Consequently, one would expect USDBRL to continue trending lower in line with anticipated rate cuts. Instead, USDBRL recently surged to levels reminiscent of the pandemic era, defying conventional expectations.

The Brazilian Monetary Committee (COPOM) was one of the earliest to react to rising inflation, initiating aggressive rate hikes as early as 2021. This preemptive stance set COPOM apart from other major central banks, which only began tightening in 2022. The much more aggressive hikes helped stabilize the BRL, leading to a sustained downtrend in USDBRL.

The COPOM has also been quick to address the recent reversal in inflation trends. A 25-basis-point rate hike in September and November signals the start of a monetary tightening cycle aimed at countering inflationary pressures, especially in food and energy prices.

Although COPOM began cutting rates in the second half of 2023, global narratives remained focused on the U.S.'s potential for a soft landing. Amid the lack of confidence in post-pandemic recovery and lack of direction in major central banks’ stance on rate hikes, capital stayed in developed markets. However, the latest cuts from major central banks suggest a shift toward more accommodative policies, potentially sparking renewed interest in riskier emerging market assets. Brazil stands to benefit from this shift, particularly following COPOM’s decision to raise rates. Yet, the recent USDBRL breakout suggests a market sentiment that is incongruent with these developments.

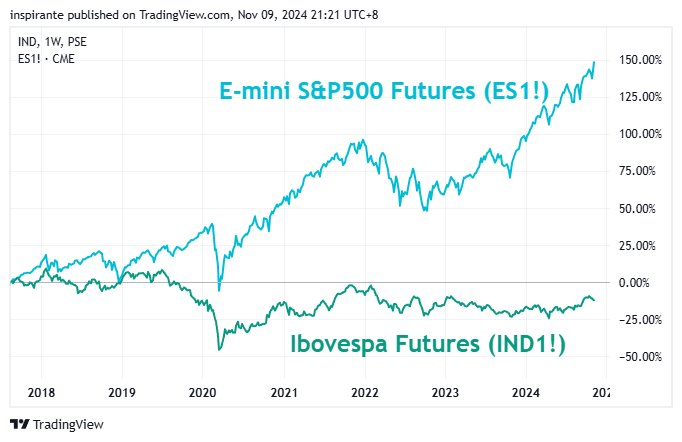

This odd occurrence extends to the equity market as well. Back in March 2024, we noted the divergence between the S&P500 and Ibovespa. While the divergence narrowed slightly after, the S&P500 benefited from the subsequent AI-driven gains, and Brazil’s Ibovespa futures lagged. This reflects a broader uncertainty surrounding Brazil’s financial outlook.

The trade balance measures the difference between exports and imports of goods and services whereas the capital flows measure the ownership of Brazilian assets by foreigners against foreign assets owned by Brazilians. This can include foreign direct investment, portfolio investment and other investments.

Despite episodes of capital outflow in 2024, Brazil’s trade surplus has been relatively stable, which has effectively provided a buffer. Throughout the first half of 2024, the net positive combined inflow signals an overall greater demand for the BRL and ought to provide additional support for the currency.

Moreover, China’s recent stimulus measures are likely to have a positive impact on Brazil. As a major commodity exporter, Brazil’s trade figures are closely tied to China’s economic performance. The announcement of China’s 2025 investment budget for construction projects is expected to further boost Brazil’s trade numbers.

Though there is different dynamics in international trade and investment, market sentiment still weighs heavily on bearish expectations on Brazil’s financial market over her strong trade capabilities.

Brazil’s central bank recently revised its 2024 growth forecast upwards, citing stronger-than-expected data. Brazil’s GDP grew by 1.4%, while real GDP expanded by 2.68%, rebounding after two quarters of stagnation. With annual GDP growth projected to hit 3% by the fourth quarter, Brazil’s economy is proving to be more resilient than market sentiment suggests.

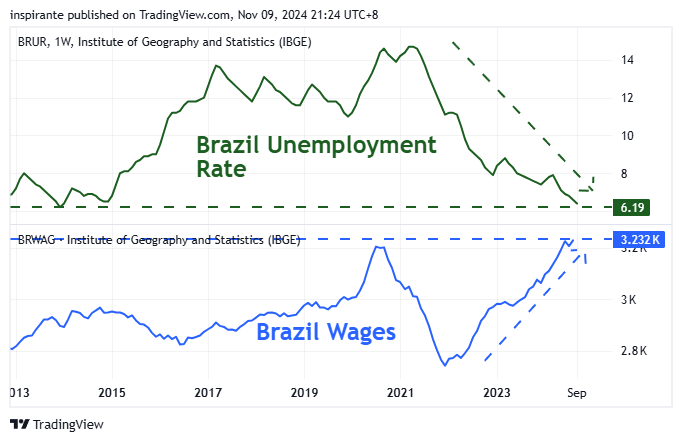

While the market panicked over U.S. unemployment rate spike in July, Brazil’s unemployment rate has been consistently declining, a clear indication in a significant improvement in labor participation rate. Furthermore, wages, benchmarked using real earnings, have shown significant recovery post-pandemic, reaching new highs. This labor market strength further supports the fundamentals of the Brazilian economy.

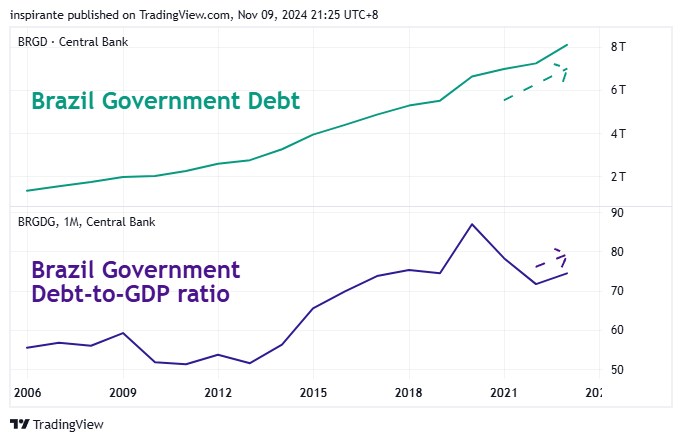

Brazil’s rising government debt and debt-to-GDP ratio have raised concerns among investors, highlighting a significant fiscal challenge. While the debt-to-GDP ratio had improved in recent years, 2023 marked a reversal suggesting a possible upward trend that alarmed markets. This is compounded by the government’s recent decision to relax budget targets for 2025 and 2026, extending the timeline to achieve fiscal surplus. Such moves signal a longer period needed to stabilize Brazil’s growing public debt, prompting fears of higher future inflation and questions about the government’s commitment to fiscal discipline. Investors worry that these factors could lead to elevated inflation expectations and erode the perceived value of Brazilian assets, demanding higher risk premiums to compensate for fiscal uncertainty.

Every Cloud has a Silver Lining

Despite these fiscal challenges, Brazil’s economy continues to demonstrate resilience. Trade surpluses remain robust, GDP growth is positive, and the labor market is strong. COPOM’s recent rate hike signals its determination to combat inflationary pressures. Brazil’s Treasury Secretary, Rogerio Ceron, has pledged to outperform fiscal targets, while Moody’s recent credit rating upgrade in October places Brazil just one notch below investment grade. This contrast between solid economic fundamentals and fiscal instability has created a situation where the market appears overly focused on Brazil’s fiscal risks, potentially mispricing the country’s overall economic health. Consequently, this divergence highlights a lopsided risk premium that investors may exploit, particularly by engaging in relative value trades on the yield curve.

Gaining Access to the Yield Curve

Brazil’s main interest rate contract, the DI Futures which is traded on the B3 exchange, reflects the expectations of the market for the average DI Rate over a specified period – starting from the trade day (inclusive) to the contract’s maturity date (exclusive). The DI Rate is the average rate for one-day Interbank Deposit Certificates (CDI) traded between different banks but, nowadays, considering their methodology and the current market dynamic, this rate has the same value of Selic Over Rate (Brazilian interest rate benchmark that will follow the Selic Target Rate). The Selic Target Rate is the interest rate set by the COPOM and used by the Brazil Central Bank in the implementation of the monetary policy. Both local and non-local investors trade the DI Futures to express their views and expectations of the Brazilian yield curve, making DI Futures one of the most liquid interest rate instruments traded globally. Furthermore, B3’s COPOM Option Public Dashboard provides a convenient visualization of such market sentiment – Selic Target Rate probabilities decided at each COPOM meeting. These probabilities are calculated with B3’s COPOM Option contracts.

All DI Futures contracts are cash settled and payout 100,000 BRL at the end. The total profit and loss will include all the daily settlement to be carried out until the expiry date. Since the DI Futures contract is quoted in rates, to express the view of a rate cut, an investor can simply short the DI Futures in the respective maturities being studied. Furthermore, by analyzing DI Futures rates across shorter maturities, investors can gauge market sentiment regarding future COPOM actions while rates across longer maturities reflect sentiments on the broader outlook on economic conditions. An example to interpret the DI Futures rates and calculate the daily settlement is provided by B3 under the topic of directional positions.

Evidently in Figure 2, the COPOM has always reacted promptly to address any reversals in inflation trend. As it is incredibly difficult to predict future inflation trends and other economic conditions, it is therefore difficult to predict COPOM’s reaction in the future. As such a directional trade on DI Futures can prove to be relatively risky.

As of 10th Nov 2024, the rates quoted by the DI1F35, expressing a 10-year view, and the DI1F27, expressing a 2-year view, are at 12.49% and 13.09% respectively, resulting in an inverted yield curve.

Considering Brazil’s strong economic fundamentals, the current inverted yield curve appears overly pessimistic. A trade, constructed with DI1F27 and DI1F35, that anticipates a normalization to a positive yield curve could be profitable. To set up the trade, we would have to calculate the sizing ratio from a Basis Point Value (BPV) neutral perspective. The computation is shown in the table below.

We would consider taking a long position on the forward rate strategy by selling 100 DI1F27 futures and buying 55 DI1F35 futures. Each basis point move in the DI1F27 leg is 100 * R$ 14,46 = R$ 1.445 and each basis point move in the DI1F35 leg is 55 * R$ 27,35 = R$ 1.504. Evidently, each basis point move in the DI rate would have roughly the same profit and loss impact on either contract. This is achieved by the BPV neutral calculation.

From Figure 9, we would place the stop-loss at -0,65, a historical support line, for a hypothetical maximum loss of 5 basis points, 5 * R$ 1.504 = R$ 7.520. Likewise, we would place the take-profit at 0,93, a historical resistance line, for a hypothetical gain of 153 basis points, 153 * R$ 1.446 = R$ 221.238.

In conclusion, this relative value trade would be more favorable. As expressed in this trade, the normalization could happen as a result from either a rise in the DI1F35, a fall in the DI1F27, or a concurrent rise and fall in the DI1F35 and DI1F27 respectively. This proves that a relative value trade is likely to be less risky as compared to a directional bet on the Selic Target Rate using one DI Futures contract.

| A guest post by

|