Addendum to “The Turning Tides”

Addendum to “The Turning Tides”

Original article:

Following our initial publication, we've received some astute feedback that warrants further and more in-depth discussion. A reader correctly noted that the DAX and Euro STOXX 50 differ in their treatment of dividends - a detail we initially glossed over for simplicity's sake. The DAX is a performance index, including dividends, while the Euro STOXX 50 is a price index, excluding dividends. Understandably, it's a distinction that does play a role in their historical performances. It's also worth noting that a more apple-to-apple comparison to the DAX Index future might be the Euro STOXX 50 Index Total Return future (TESX). However, we originally chose the more popular FESX future due to its better liquidity and much longer history (TESX was only launched in 2016). In addition, the availability of Micro future contracts also makes it more retail-friendly.

Our primary exploration focused on overarching macroeconomic factors and sectoral shifts, which are pivotal to understanding the relative performance between the indices. However, dividends' contribution to long-term performance is undeniably significant. Therefore, it is prudent to revisit our DAX-to-STOXX50 comparison, this time adjusting for dividends.

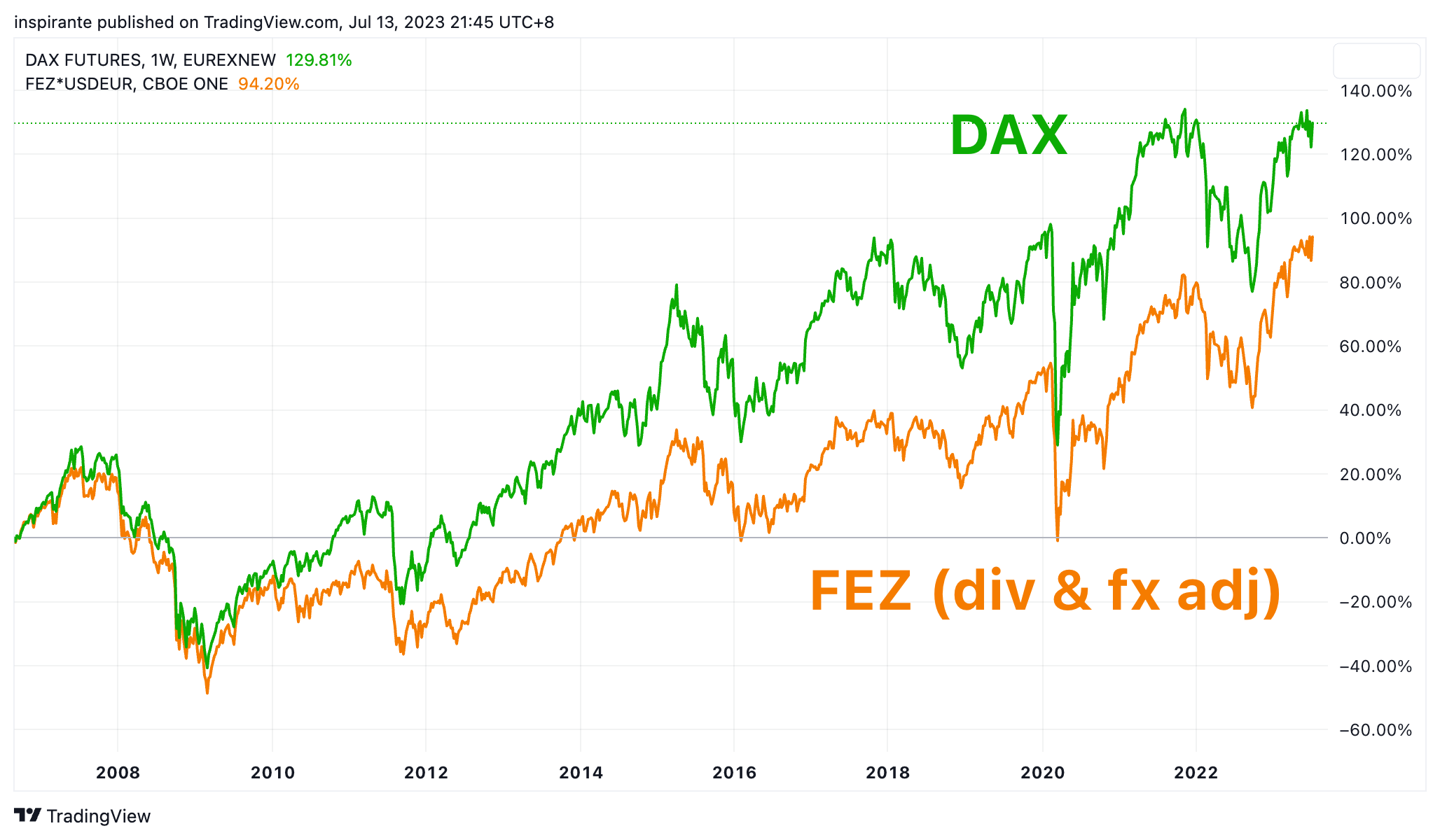

For this purpose, we've chosen the SPDR® EURO STOXX 50® ETF (FEZ) as a proxy for a dividend-adjusted STOXX50. The ETF seeks to provide investment results that, before fees and expenses, generally correspond to the total return performance of the STOXX50 Index, and it has been around since 2002. One thing to note about FEZ is that it's USD-denominated; therefore, we need to consider the EUR/USD exchange rate move over the years to get as close a proxy as possible.

Here's an updated DAX vs. dividend and exchange rate-adjusted STOXX50 ETF chart. The revised perspective still affirms DAX's relative outperformance over the past decade, although less pronounced than the FDAX vs FESX futures comparison suggests.

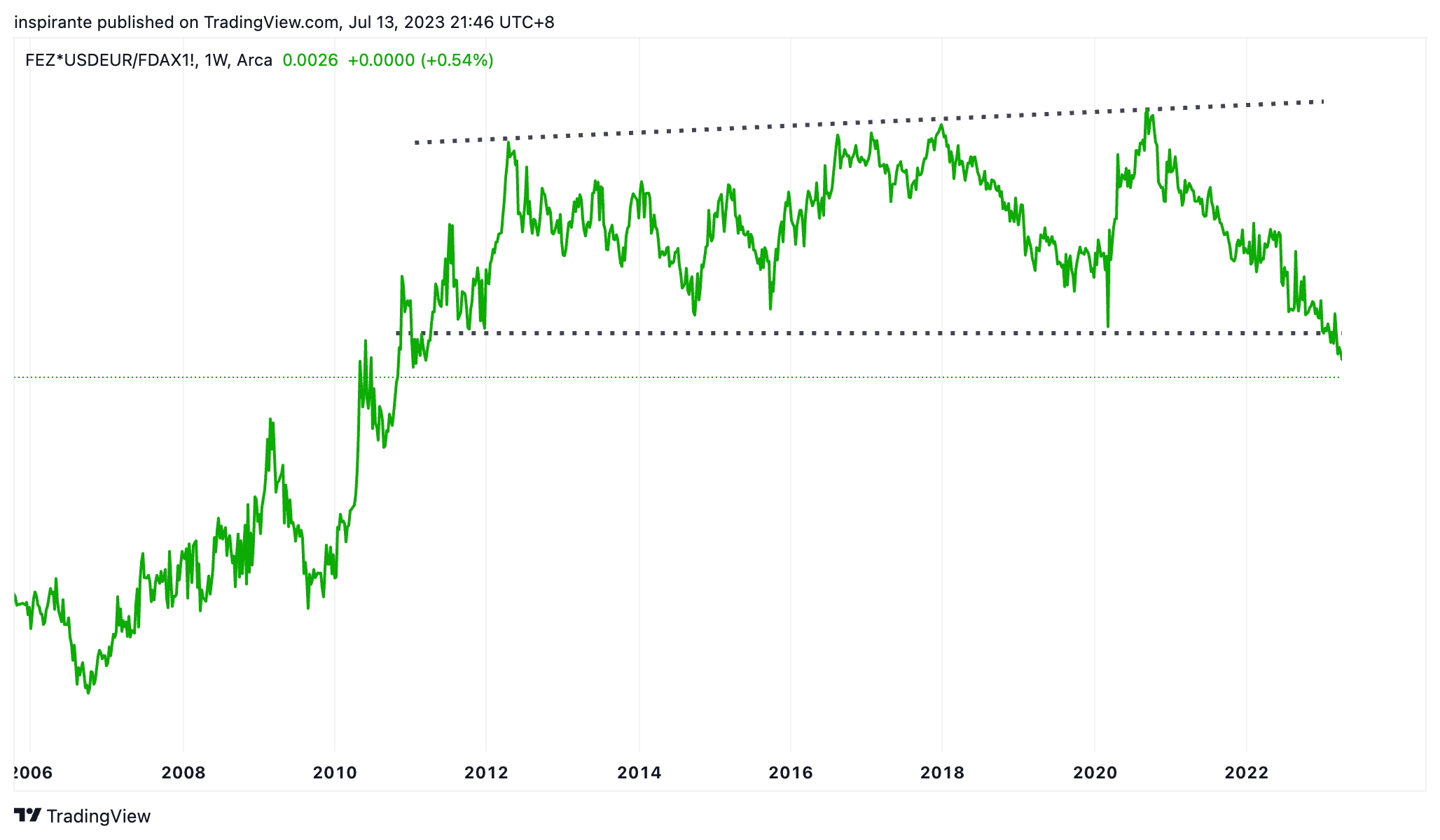

On a closer look at the ratio between the DAX and the dividend-adjusted FEZ, a clear and massive topping pattern emerges, and it has arguably already broken the neckline support. In other words, it appears that the DAX is likely going to continue underperforming the STOXX50 on a dividend-adjusted basis. Our initial analysis and conclusion on the relative performance of the German DAX index vs a broader European STOXX50 index still hold.

This finer detail serves as a reminder of the multifaceted complexity within financial markets and the multitude of factors influencing asset performance. It also underscores the invaluable contribution of reader feedback, enabling us to deliver deeper, more nuanced market analyses. We deeply appreciate your active engagement and eagerly anticipate further enriching discussions.

| A guest post by

|