A cut, pause & hike.

Flipping through the markets

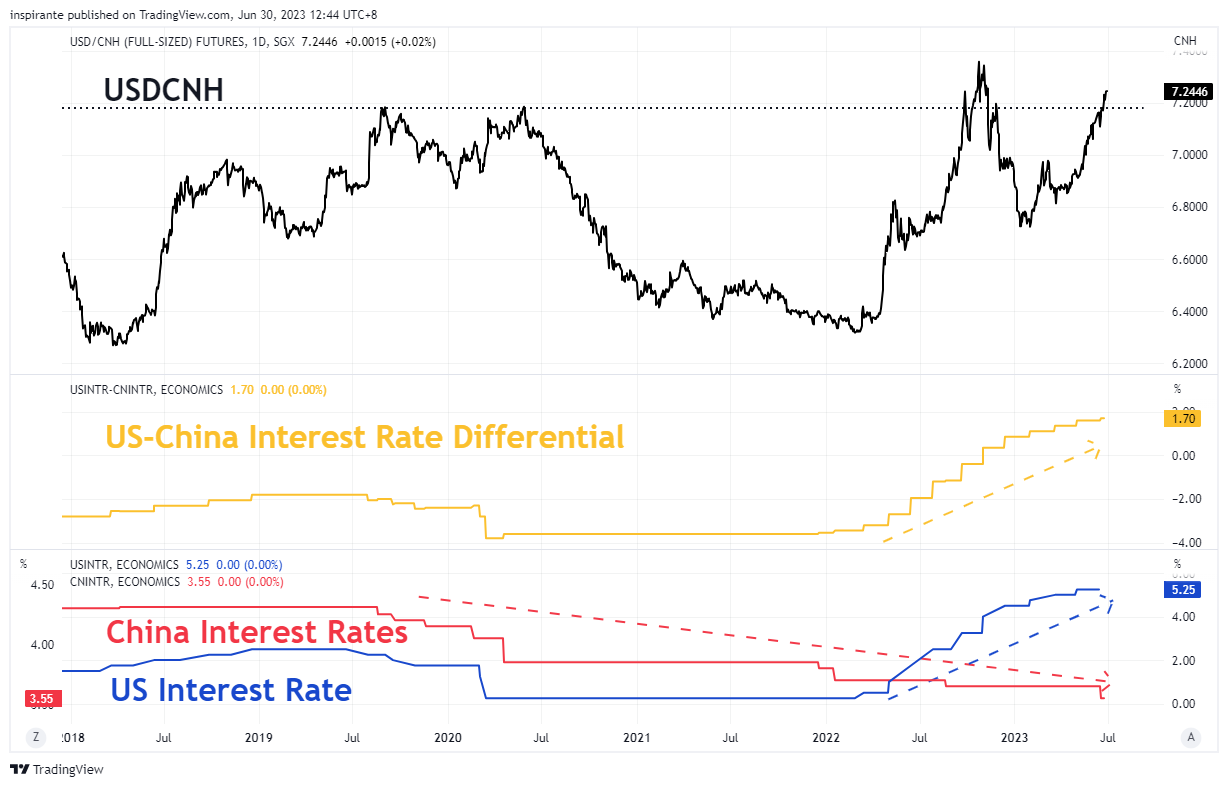

China seems to be struggling and the central bank knows it. Across many of the data points, we see a slump well on its way. New orders are creeping back into negative territory, consumer confidence is at a low, and exports numbers in May plunged to -7.5%. As a superpower, this slowdown has significant effect on others…

China's response to its economic slowdown is a rate cut, contrasting with the US Federal Reserve's "hawkish pause." Futures implied forward rates and the Fed's dot plot suggest further hikes in the US, implying that the interest rate differential between the US and China is set to grow. This has contributed to the weakening of the Chinese Yuan (CNH), which is breaking past previous resistance levels, although it hasn't yet reached its 2022 highs

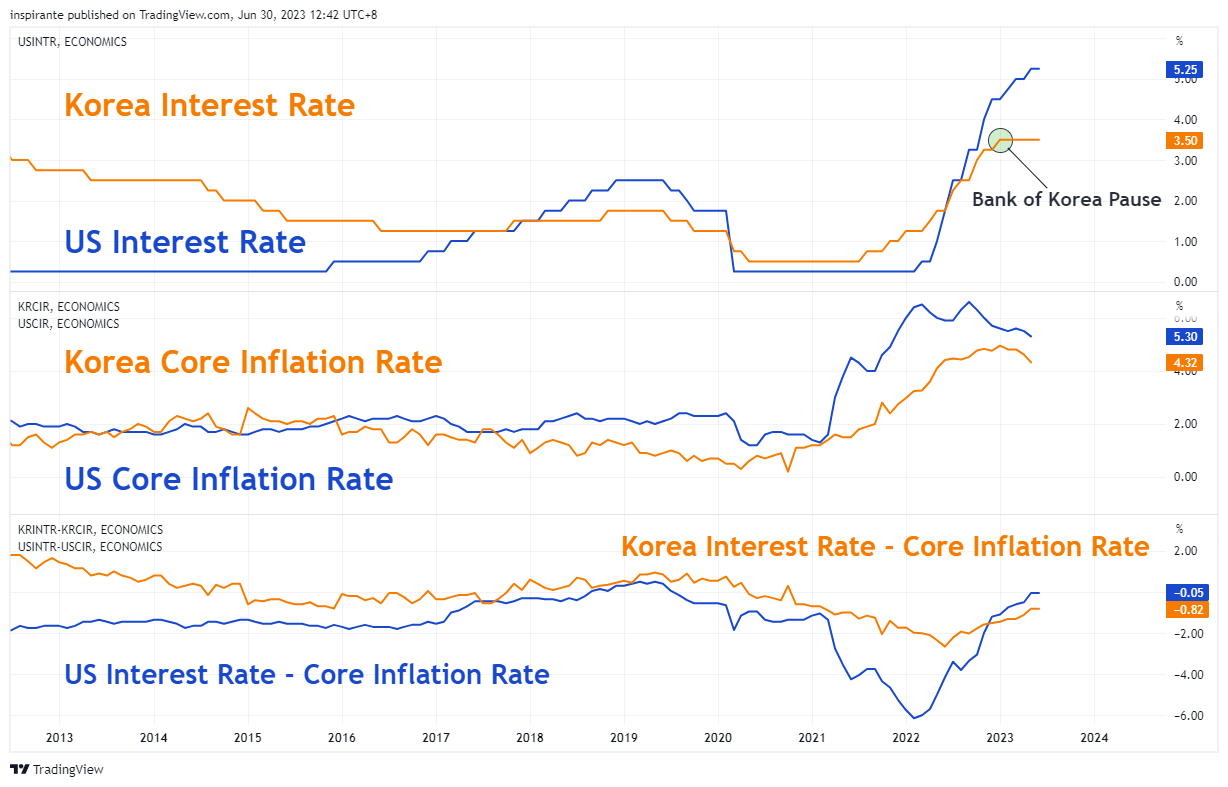

The Bank of Korea has paused its rate hikes for three consecutive meetings as it gauges the country's battle with inflation. Despite these pauses, core inflation remains persistently high, leading to 'real rates' in Korea lagging behind those in the US. This situation is particularly significant given that the Bank of Korea has communicated that it is open to a terminal rate of 3.75%

The Korean Won (KRW), which traditionally trades in close correlation with the dollar index, has started to diverge, with the KRW trading 'weaker.' This could be due to the impact of lower real rates. However, with the Bank of Korea meeting scheduled for July and core inflation remaining a concern, a hike may be forthcoming.

We can also examine the KRWCNH pair by synthetically constructing it using the KRWUSD and USDCNH pairs. This method allows us to express the relative strengthening of the KRW and weakening of the CNH without any exposure to the dollar. The KRWCNH now trades right on the support as it slowly grinds higher…

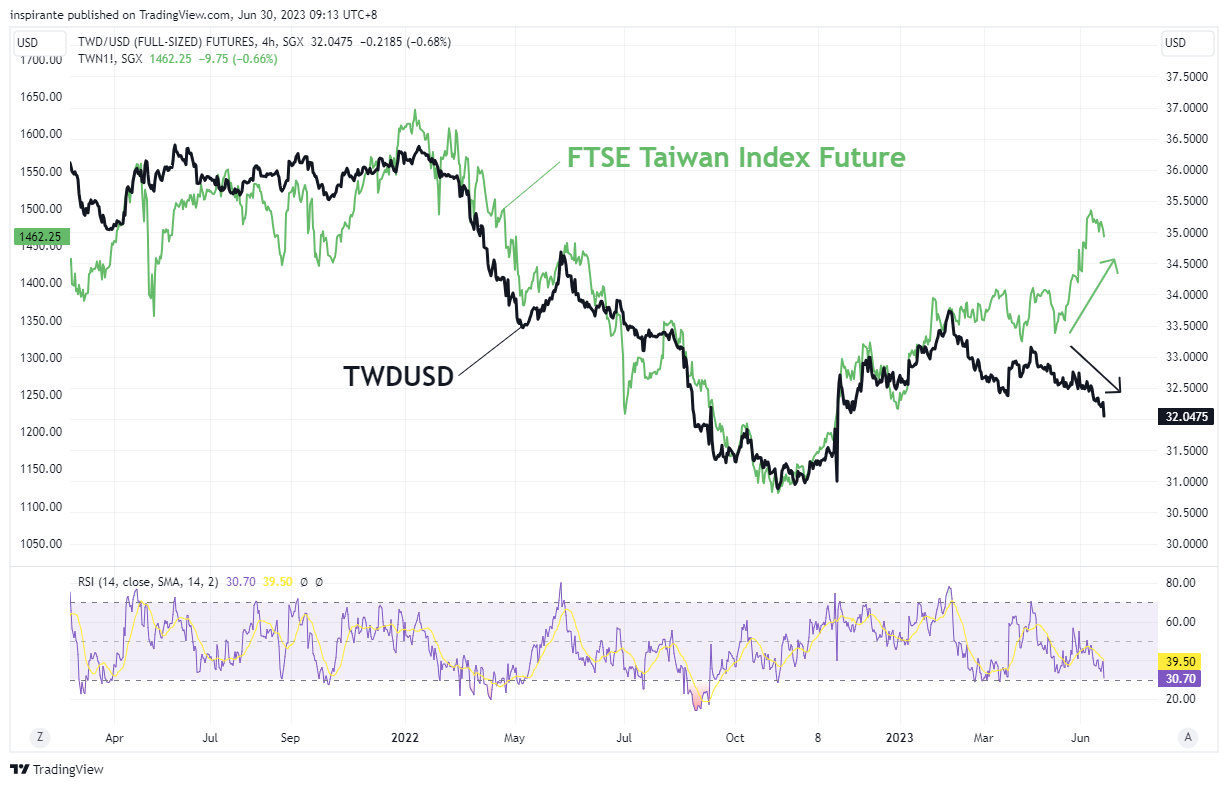

Since 2022, the Taiwanese Dollar (TWD) has been trading in sync with the FTSE Taiwan Index Future. However, this correlation began to diverge in February. Weak exports due to softer demand from the US and Europe, along with low inflation, are some of the reasons communicated for the central bank's decision to pause its rate hikes.

What’s inside our playbook?

After an action-packed central bank meeting schedule in June, where the US Federal Reserve paused for the first time, ECB continues its hiking path, and the BOE hiked above expectations, we thought it would be apt to focus this month's market overview on the topic at hand.

The central theme revolves around the contrast in monetary policy stances adopted by major central banks amid diverging economic situations. The three cases in point are the United States, China, and South Korea, each demonstrating a unique set of challenges and responses in the face of global economic uncertainty.

China, the world's second-largest economy, appears to be entering a phase of deceleration, with key economic indicators such as new orders and consumer confidence slipping into negative territory and export figures reflecting a significant drop. This has prompted the Chinese central bank to adopt a rate-cutting approach, a move that seems to signal an attempt to stimulate economic activity and ward off a more severe slowdown.

South Korea presents an interesting case. The Bank of Korea has hit the pause button on its rate hikes for three consecutive meetings as it assesses its inflation situation. Core inflation remains high, and 'real rates' in Korea have slipped behind those in the US. The Korean Won (KRW) is trading weaker relative to the dollar index, possibly reflecting the impact of lower real rates. However, with a Bank of Korea meeting due in July and core inflation still a concern, a hike may be on the cards, especially considering their communication about a potential terminal rate of 3.75%. We see this as a very similar situation to the US with Korea being just slightly ‘ahead’ in terms of schedule.

On the other hand, the US Federal Reserve's stance is somewhat hawkish, albeit in a paused state. Despite the overall global economic uncertainty, the US economy is demonstrating resilience, and the Fed is looking toward future rate hikes. The forward rates indicated by futures and the Fed's dot plot are suggestive of this trajectory. This policy divergence with China is leading to an expanding interest rate differential and a consequent weakening of the Chinese Yuan (CNH) against the US dollar.

These divergent central bank policies reflect the complexities of global economic interdependencies. They highlight the delicate balancing act central banks must perform, navigating between stimulating growth and controlling inflation, all while being cognizant of their actions' ripple effects on global economies. As traders, understanding these dynamics and their implications on currency and equity markets can provide valuable insights and potential trading opportunities.

Executing the plays

A hypothetical investor can consider the following two trades1:

Case Study 1: Long SGX USD/CNH FX Futures (UC)

We would consider going long on the USD/CNH given the weakening outlook on China and a still hawkish US federal reserve. This view can be expressed using either the SGX USD/CNH FX Futures Full-Sized (UC) or Mini (MUC) contracts, where each 0.0001 move is equal to 10 CNH for the full-sized contract and 2.5 CNH for the mini contract. From the current level of 7.245, a tighter stop at 7.190 and take profit at 7.345 will give us a reasonable risk-reward of roughly 2:1.

Case Study 2: Long SGX KRW/USD FX Futures (KRW)

We would consider taking a long position on the KRW/USD given the likelihood of the Bank of Korea reacting to still high inflation after a few rounds of pause. This view can be expressed using the SGX KRW/USD FX Futures Full-Sized (KRW) or Mini (KU) contracts, where each 0.00005 move is equal to 6.25 USD for the full-sized contract and each 0.0001 move is equal to 2.5 USD for the mini contract. From the current level of 0.7580, we will take a risk-measured stop at 0.7453, slightly below a previous level of support, and take profit at 0.7885.

Original Link: https://www.sgx.com/research-education/market-updates/20230630-sgx-traders-playbook-cut-pause-hike

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.

| A guest post by

|