A rising yield on the land of the Rising Sun

First published on 2023-01-18

Markets in Focus

As headline inflation numbers started to cool off in the US and recession fears permeated the market, the greenback has nosedived to below 104. However, it remains to be seen whether the breakdown from this significant resistance-turned-support level is a false break or the decline will have more room to go in the following weeks.

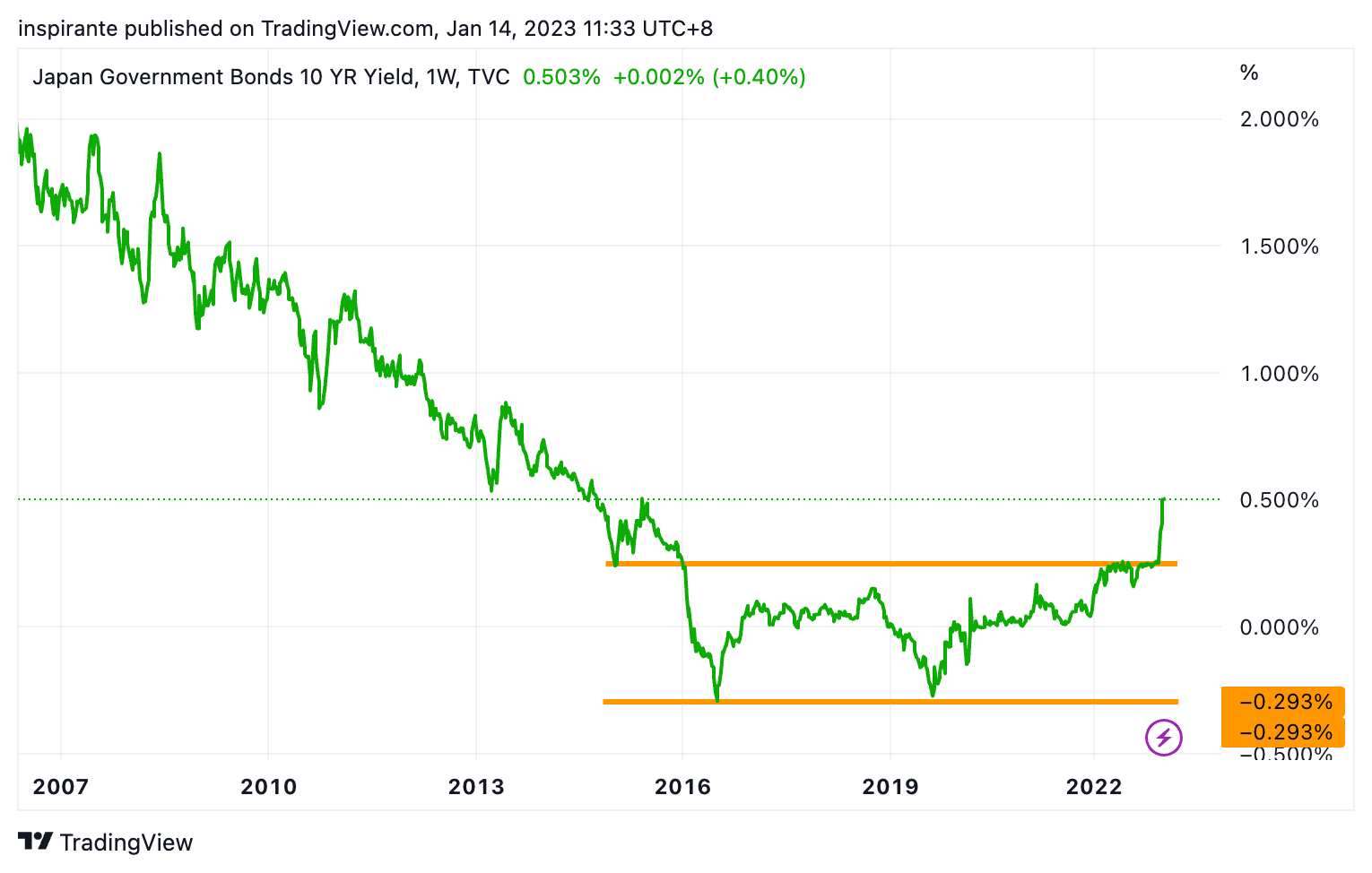

Japan’s 10-year yield finally broke out from the previous mandated band after the Bank of Japan (BoJ) unexpectedly changed its Yield Curve Control (YCC) policy in its December meeting. Market participants are debating if the BoJ will implement further adjustments to allow bond yields to go higher.

Many investors have regarded AUD/JPY as the global risk-on/risk-off signal. It has been trading in a well-defined descending triangle since 1985. Last year, on Yen’s notable weakness, this pair reached the triangle’s upper resistance. It is turning lower, however, especially as Yen started to strengthen due to BoJ’s policy shift.

The ratio between the Tokyo Stock Price Index (TOPIX) and the Nikkei 225 Index has been trading in a persistent downtrend since 2006. Its move has been highly correlated with the move of the Japan 10-year yield. This ratio also started turning higher lately.

Our Market Views

In our very first piece of 2023, we sincerely wish every reader a fruitful and prosperous new year! With many crosscurrents in the macro landscape, the market is more challenging than ever to navigate. However, we believe the uncertainties also bring plenty of exciting opportunities ahead, so long as we keep a cool head and manage the risks well.

Speaking of market risks, we think the new year’s first major macro event will likely come from the land of the Rising Sun. Japan is an economy that did not get much attention for the better part of the last three years. In 2021 and 2022, the Japanese equity market behaved much more calmly than the US or many other countries by trading sideways, nothing like the Nasdaq’s rollercoaster ride. By any measure, the USD/JPY pair experienced a significant upmove in 2022. Again, the story did not get the much-deserved coverage because 2022’s forex headlines were predominantly about the broad and relentless rally of the US Dollar against all other currencies. 2023 is the year investors should really pay more attention to Japan, especially its central bank’s policy decisions, as those will have a meaningful impact on the global financial markets.

In the last scheduled meeting of 2022, the BoJ surprised the entire market by widening the band of the Japan 10-year yield, the first time since they implemented the YCC in September 2016. This decision could result from many reasons, such as inflation picking up meaningfully in Japan and the ever-increasing yield differentials between Japan and the rest of the world which has put tremendous pressure on the Japanese Yen. Suddenly, there are many speculations in the market on whether the BoJ will again adjust its monetary policy, potentially as early as in their first meeting on Jan 17th.

We are not sure if the BoJ will have another policy shift so soon, given headline inflations in many countries seem to have peaked in Q4 last year and started to cool down thanks to a much-needed weaker greenback. Nevertheless, we think longer term Japan will converge with the rest of the world to have a higher bond yield. In that scenario, the Japanese Yen has the potential to strengthen further as the yield differentials narrow. To express this view without outright exposure to the US Dollar, we could consider a cross between Yen and another currency, such as AUD/JPY shown in Figure 3. A relative outperformance of the Yen to the Aussie would mean this pair continues its reversal after being rejected at the multi-decade overhead resistance.

We are also interested in the relative performance of two Japanese indices, the TOPIX and the Nikkei 225. These two have different weighting mechanisms, i.e., the TOPIX is market cap-weighted, whereas the Nikkei is price-weighted. Hence, the TOPIX is generally more sensitive to bond yields than the Nikkei as it is heavier in financial stocks. A rising yield and a potentially steeper yield curve benefit Japanese financial institutions. The long-term trend of the relative performance of these two indices may finally reverse from here.

How We Express Our Views

We consider expressing our views via the following hypothetical trades1:

Case Study 1: Short AUD/JPY Future

We would consider taking a short position on AUD/JPY March 2023 future (AJYH3) at the present level of 88.4, with a stop-loss at 100, which could bring us a hypothetical maximum loss of 11.6 points. Looking at Figure 4, if the overhead resistance holds and the reversal continues, this pair has the potential to fall back to 70, a hypothetical gain of 18.4 points. Each point move in the AUD/JPY future contract is JPY 200000.

Case Study 2: Long TOPIX/Nikkei Ratio

We would consider taking a long position on the synthetic TOPIX/Nikkei ratio at the present level of 0.0732, (by taking a long position in TOPIX March 2023 future (TPYH3) at 1889 and a short position in Nikkei 225 March 2023 future (NIYH3) at 25800 for notionally equivalent amount) with a stop-loss below 0.068, which could bring us a hypothetical maximum loss of 0.0052 points. Looking at Figure 3, if the trend reversal continues with the rising yield, this ratio has the potential to reach 0.08, a hypothetical gain of 0.0068 points. Each point move in the TOPIX future contract is JPY 5000, and each point move in the Nikkei future contract is JPY 500.

Original Link: https://www.cmegroup.com/newsletters/fresh-from-the-trading-room/2023-01-18.html

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios. Please refer to full disclaimers at the end of the commentary.

| A guest post by

|