A Wild Ride in Japan

Written on 2024-10-03, first published on 2024-10-08

Markets in focus

In the past few months, the volatility of the Nikkei 225 index has reached an all-time high and has since been trading at an elevated level. The price has been consolidating.

Following a series of decisions taken by the BOJ and Fed, USD/JPY’s breakout below a multi-year support line has confirmed a regime change.

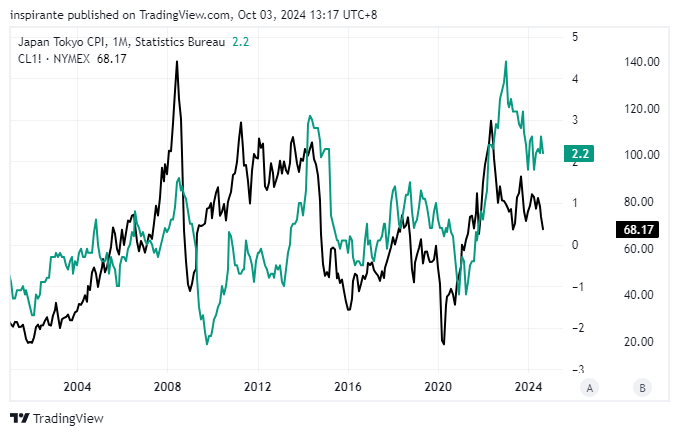

Japan is a top importer of energy with crude oil being a major component of its imports. The prices of crude oil seem to be positively correlated to Japan’s CPI prints.

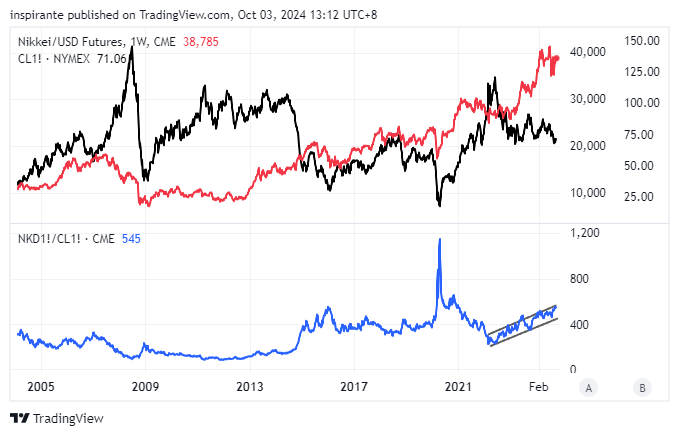

The USD-Denominated Nikkei 225 to Crude Oil ratio is at the upper resistance of a multi-year ascending channel. Amid evolving geopolitical tensions in the Middle East and the appointment of Japan’s new prime minister, who has a hawkish monetary stance, the bias for the ratio appears tilted towards potential downside, increasing the likelihood of a pullback.

Our market views

The past few months have been a rollercoaster ride for Nikkei 225 traders. Since the beginning of the year, the index steadily climbed higher, driven by strong corporate earnings, positive economic data, and a broader rally in global markets. This momentum saw the Nikkei surpass its 1989 peak. However, on August 2nd, the market faced a sharp reversal triggered by a sudden rise in U.S. unemployment and a perceived hawkish tilt in Japan’s long-standing accommodative monetary policy. This unwinding of carry trade resulted in the largest one-day point drop for the index. While most of the losses were quickly recovered, optimism soon dissipated due to recession concerns in the U.S. and a strengthening yen. Given the U.S. is a critical market for Japanese exports, weaker-than-expected U.S. manufacturing data signaled potential softness in demand for Japan’s products.

Further uncertainty came with the election of Japan’s new prime minister, creating tension among investors due to the stark differences in fiscal and monetary policies among leading candidates. On one side, Shigeru Ishiba expressed support for monetary policy normalization and potential increases in capital gains and corporate taxes. On the other, Sanae Takaichi criticized Bank of Japan’s (BOJ) recent hikes and advocated for continued monetary easing. Leading up to the September 27th election, markets rose on the prospect of Takaichi winning, only for these gains to be wiped out when Ishiba ultimately took office, disappointing those who had expected continued easing.

The normalization of Japan’s monetary policy, combined with the Federal Reserve’s 50-basis-point rate cut, has narrowed the rate differential between the two nations. This shift led to the USD/JPY breaking below its multi-year support line, signaling a regime change in the currency pair.

“Personally, I think now is not the right environment for an additional rate hike,” Ishiba commented after talks with BOJ chief Kazuo Ueda. Similarly, Fed chairman Jerome Powell remarked, “We are not on any preset course”, suggesting that policymakers would base future decisions on forthcoming economic data and the market should not expect a 50-basis-points cut going into each meeting. While neither the BOJ nor the Fed is rushing to make further adjustments, long-term market participants understand that surprise actions from the BOJ cannot be ruled out. Ueda’s view that Japan’s current policy is “extremely accommodative” hints at the possibility of future rate hikes, while new evidence of a looming U.S. recession could spur the Fed to cut rates faster than anticipated.

A stronger currency, while beneficial in some ways, can also pose challenges. A rising yen reduces import costs for domestic companies, but it also squeezes profit margins for exporters, a critical segment of Japan’s economy. As a net exporter, Japanese companies are more likely to feel the impact from yen appreciation. This sentiment aligns with the broader market, as reflected in the stock market's decline when Ishiba took office.

Japan, a major importer of energy, is especially vulnerable to fluctuations in oil prices, with crude oil being a significant component of its imports. The escalating tensions in the Middle East have pushed crude oil prices higher, and with increased volatility expected, Japan’s trade balance and corporate profits, particularly in energy-intensive industries, could suffer. Higher oil prices would also affect consumers, potentially driving inflation higher.

In conclusion, Japan’s equity market is facing pressure from multiple angles. The possibility of further BOJ rate hikes could lead to yen appreciation, eroding Japan’s export competitiveness and capping corporate profits. At the same time, higher oil prices would increase costs, further compressing margins and limiting corporate net incomes. These challenges, combined with potentially higher inflationary pressures, could fuel the need for more aggressive rate hikes, which would strengthen the yen further. The culmination of these factors supports a bullish outlook for the yen but a bearish tone for the Nikkei 225 index.

However, it is imperative to be mindful of the October Effect. Historically, October tends to be more volatile than other months, and this year the uncertainty is likely magnified by Japan’s general election on October 27th and the U.S. presidential election on November 5th. The outcomes of these elections could drastically alter market dynamics. Hence, we favor a relative value trade between the Nikkei 225 index and crude oil. Years of extremely accommodative monetary policy by the BOJ against other major central banks’ post-pandemic restrictive stance have left this ratio relatively overvalued. Given the shift in BOJ and Fed monetary policies and heightened geopolitical tensions now, this overvaluation should begin to correct.

How do we express our views?

We consider expressing our views via the following hypothetical trades1:

Case study 1: Short USD-Denominated Nikkei 225 to Crude Oil ratio

To express the view that market is overpricing the Nikkei 225 index to crude oil ratio, we would consider taking a short position in the Nikkei 225/ Crude Oil ratio, by simultaneously selling one USD-Denominated Nikkei Futures (NKDZ4) at 38,785 and buying three WTI Crude Oil futures (CLZ4) at 71.06, with an effective price ratio of 38,785/ 71.06 = 545.8. We would put the stop-loss above 560, the upper band, which could bring us a hypothetical maximum loss of 545.8 – 560 = 14.2 points. Looking at Figure 4, the ratio has the potential to traceback to the lower band of 445, a hypothetical gain of 545.8 – 445 = 100.8 points. Each point move in Nikkei (USD) futures contract is 5 USD, and each point move in the WTI Crude Oil futures is 1000 USD. Therefore, we will need a ratio of 1: 3 between Nikkei 225 futures an WTI Crude Oil futures to make the two legs of this trade dollar neutral.

· Leg 1: short 1 NKDZ4 at 38,785

Notional value: 38,785 x $5 = $193,925

· Leg 2: long 3 CLZ4 at $71.06

Notional value: $71.06 x 1000 x 3 = $213,180

We can look at two hypothetical scenarios to understand the approximate dollar value of a 1 point move in ratio.

Scenario 1: Assuming the Nikkei (USD) stays unchanged, and the Crude Oil falls to 70.93 and the ratio becomes 38,785/ 70.93 = 546.8. The overall loss, which comes solely from the Crude Oil position in this case is ($71.06 - 70.93) x 1000 x 3 = 390 USD.

Scenario 2: Assuming the Crude Oil stays unchanged, and the Nikkei (USD) falls to 38,713 and the ratio becomes 38,713/ 71.06 = 544.8. The overall profit, which comes solely from the Nikkei (USD) position in this case is (38,785 – 38,713) x $5 = 360 USD.

In Scenario 1, the ratio increases by 1 point, yielding a loss of 390 USD from the long Crude Oil position. In Scenario 2, the ratio decreases by 1 point, yielding a profit of 360 USD from the short Nikkei (USD) position.

We could consider expressing the same view via the micro sized contracts. While Micro Nikkei 225 futures contract is scheduled to launch on October 28th, Micro WTI Crude Oil futures are readily available. These micro contracts allow traders to capture trading opportunities with greater flexibility and precision. Both micro futures contracts are 1/10 the size of the standard contracts.

Case study 2: Long JPY/USD Futures

We would consider taking a long position in the JPY/USD futures (6JZ4) at the current price of 0.00689, with a stop-loss below 0.00657, a hypothetical maximum loss of 0.00689 – 0.00657 = 0.0032 points. Looking at Figure 2, at the peak of Fed’s hiking cycle, the JPY/USD fell by approximately 30%. With the regime shifting for both Japan and U.S., the JPY/USD has the potential to climb back to 0.00769, resulting in a potential profit of 0.00769 – 0.00689 = 0.0080 points. Each JPY/USD futures contract represent 12,500,000 JPY, and each point move is 12,500,000 USD. E-mini and Micro JPY/USD futures contracts are available at ½ and 1/10 of the standard size.

EXAMPLES CITED ABOVE ARE FOR ILLUSTRATION ONLY AND SHALL NOT BE CONSTRUED AS INVESTMENT RECOMMENDATIONS OR ADVICE. THEY SERVE AS AN INTEGRAL PART OF A CASE STUDY TO DEMONSTRATE FUNDAMENTAL CONCEPTS IN RISK MANAGEMENT UNDER GIVEN MARKET SCENARIOS. PLEASE REFER TO FULL DISCLAIMERS AT THE END OF THE COMMENTARY.

| A guest post by

|