Barrel Bonanza

Barrel Bonanza

Written on 2023-04-08, first published on 2023-04-12

Markets in focus

Gold's recent rally, surging above $2000 and nearing its all-time high, has finally spurred silver to break free from its three-year downtrend. Having arguably completed a symmetrical triangle, silver's path of least resistance now appears to be on the upswing.

Following the unexpected OPEC+ production cut, crude oil prices gapped up over 6% when the market opened on Monday. Now trading above $80, oil is challenging a significant four-month resistance level, with a break above it potentially signaling a reversal of its nine-month downtrend.

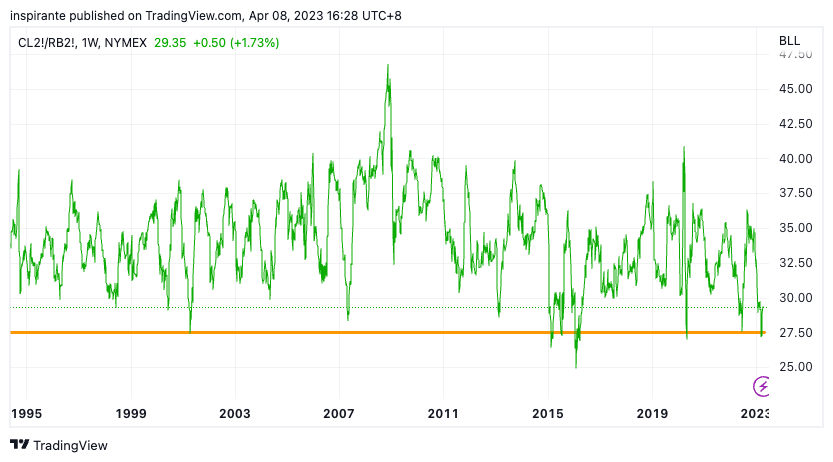

Historically, crude oil and gasoline prices exhibit a strong correlation. The recent months have been a rare exception, with crude oil notably underperforming gasoline. Nonetheless, we anticipate the close relationship between these two vital and interconnected energy products to persist.

Historically, the ratio between crude oil and gasoline prices has remained within a stable range of 28 - 40. At present, this ratio is among the lowest in history.

Our market views

In a world brimming with uncertainties, OPEC+ members dropped a bombshell last Sunday with voluntary production cuts, rocketing crude oil prices over 6% at market opening on 3rd April. Far from a flash in the pan, the front-month WTI crude oil price held steady above $80 all week long.

The labor market, on the other hand, stands strong as Friday's Non-farm Payrolls number notched an 11th consecutive beat, and unemployment hovers at a historically low 3.5%. Though the labor market is cooling, it's not icy enough for the Fed to swerve from its hawkish monetary policy, as we've underscored many times in previous publications.

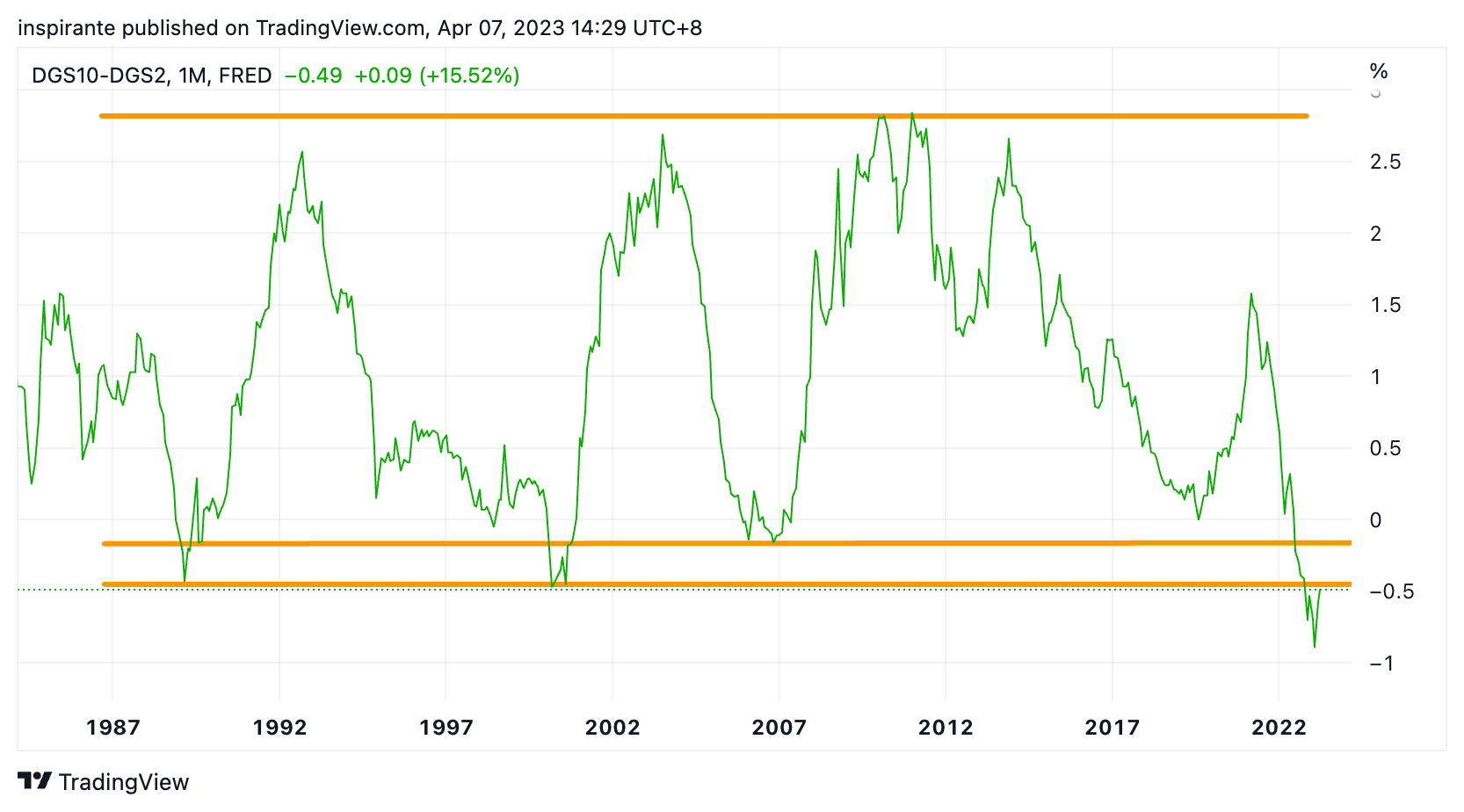

The banking sector continues to experience stress. Deposits are rapidly leaving US banks for Money Market funds, enticed by their higher yields. If this bank run continues, the risk of a systemic crisis seems increasingly concerning. The inverted yield curve has banks holding on tight, unwilling to raise deposit rates and take a hit on profit margins. How long can the Fed stay hawkish in this predicament?

As the saying goes, when it rains, it pours. The Federal Reserve must be feeling the pressure! The unexpected crude oil production cut revives a notorious inflation culprit: soaring energy prices. The ripple effect reaches beyond crude oil, impacting gasoline prices and even edible oils. Just as the world started to hope inflation was finally backing down, the energy market's latest plot twist leaves policymakers juggling a fresh batch of uncertainties.

If (and it's one colossal IF) the Fed decides to pivot in response to the banking turbulence and pumps more liquidity into the financial system, the greenback could keep sliding, paving the way for battered commodities like energy and precious metals to make a dazzling comeback.

How do we express our views?

We consider expressing our views via the following hypothetical trades1:

Case study 1: long crude oil/gasoline ratio

We would consider taking a long position on the crude oil/gasoline ratio by simultaneously buying 14 Micro WTI Crude Oil future (MCLM3) at the present level of 80.4 and selling 1 RBOB Gasoline futures (RBM3) at the present level of 2.74, at a price ratio of 29.34. The quantity ratio approximately equates the notional dollar amount for both sides of the trade (14 x 80.4 x 100 = USD 112560 for MCL and 2.74 x 42000 = USD 115080 for RB). We would have a stop-loss below 24, which could bring us a hypothetical maximum loss of 5.34 points. Looking at Figure 3 and Figure 4, if crude oil starts to catch up with gasoline, this ratio has the potential to reverse back to 35 and above. Each point move in the Micro WTI Crude Oil future contract is USD 100, and each point move in the RBOB Gasoline future contract is USD 42000.

Case study 2: long silver future

We would consider taking a long position on the silver future (SIK3) at the present level of 25.13, with a stop-loss below 23, which could bring us a hypothetical maximum loss of 2.13 points. Looking at Figure 1, if the symmetrical triangle breakout is confirmed and the rally continues, silver has the potential to reach 30, a hypothetical gain of 4.87 points. Each point move in the silver future contract is USD 5000.

The Rearview Mirror

A look into history could help us position ourselves better for the future. This section provides a rundown of market moves across major asset classes between January and March.

The US equity market has experienced a substantial upswing since hitting a low last October. For the S&P 500 index, the 4200 region represents a significant resistance level that bulls must surpass in order for the rally to sustain its momentum.

The large-cap Dow Jones index has been forming a bull flag over the past five months. The next leg of the rally will only commence once it decisively breaks above the 34000 level.

At the onset of 2023, the ratio between the Nasdaq and Dow Jones indices reached the long-term trendline. As expected, this trendline served as significant support, halting the decline and sparking a sharp reversal since that point.

The US dollar failed to breach the 106 level in its recent attempt, retreating to critical support above 100. This pullback follows a stress in the US banking sector and the market's keen anticipation of a potential "Fed Pivot."

The GBP/USD's downside breakout in early March proved to be a false break. Prices swiftly rebounded, and the currency pair is now attempting to break the upper resistance.

USD/JPY is shaping up a potential Head-and-Shoulders (H&S) top formation. The appointment of a new BoJ Governor and possible changes to the yield curve control (YCC) policy could serve as catalysts for Yen strengthening, causing this pair to decline further.

Gold concluded the week above $2000, just shy of its all-time high recorded in August 2020. This proximity suggests potential resistance and selling pressure in the $2000 - $2100 region. The initial easy rally is likely behind us; we expect an intensified battle between bulls and bears at this critical juncture.

Gold in GBP has decisively broken out from the neckline of a Cup-and-Handle pattern. Despite a period of consolidation, the upward momentum appears to remain unwavering.

The oscillation of the Kansas City vs. Chicago Wheat spread has intensified in recent years. After reaching a historic low in 2020, the spread experienced a sharp rally, swinging to the opposite extreme and hitting an all-time high.

The OPEC+ production cut news, which propelled oil prices up by over 6%, has affected edible oils. Although soybean oil experienced a short-term rally, it failed to reverse the overall decline. The soybean oil price has now retreated to the crucial support level at 55.

Corn has been trading within a massive symmetrical triangle since 2022. We anticipate a breakout soon as the price range compresses and approaches the triangle's apex.

Live cattle has maintained a perfect upward channel since 2022. The most recent rally has been remarkable in speed and magnitude, bouncing from the lower support and reaching the upper resistance.

The relentless decline of the 2-year T-Note future price (indicating a rise in yield) experienced a sharp reversal following the collapse of Silicon Valley Bank, signaling stress in the US banking sector. Interestingly, this reversal occurred at the same level that marked the bottom for the 2-year T-Note future (peak in yield) during the Great Financial Crisis.

The US 10y-2y yield curve has reached its most inverted state since the 1980s. This pronounced inversion highlights US banks' challenges, which cannot raise deposit rates to match short-term Treasury yields without compromising profitability. Encouragingly, there are signs that the curve may begin to steepen from this point onward.

Link to CME article: https://www.cmegroup.com/newsletters/fresh-from-the-trading-room/2023-04-12.html

EXAMPLES CITED ABOVE ARE FOR ILLUSTRATION ONLY AND SHALL NOT BE CONSTRUED AS INVESTMENT RECOMMENDATIONS OR ADVICE. THEY SERVE AS AN INTEGRAL PART OF A CASE STUDY TO DEMONSTRATE FUNDAMENTAL CONCEPTS IN RISK MANAGEMENT UNDER GIVEN MARKET SCENARIOS. PLEASE REFER TO FULL DISCLAIMERS AT THE END OF THE COMMENTARY.

| A guest post by

|