Capitalizing on India-China Divergence

Capitalizing on India-China Divergence

First published on 2023-10-04

Flipping through the markets

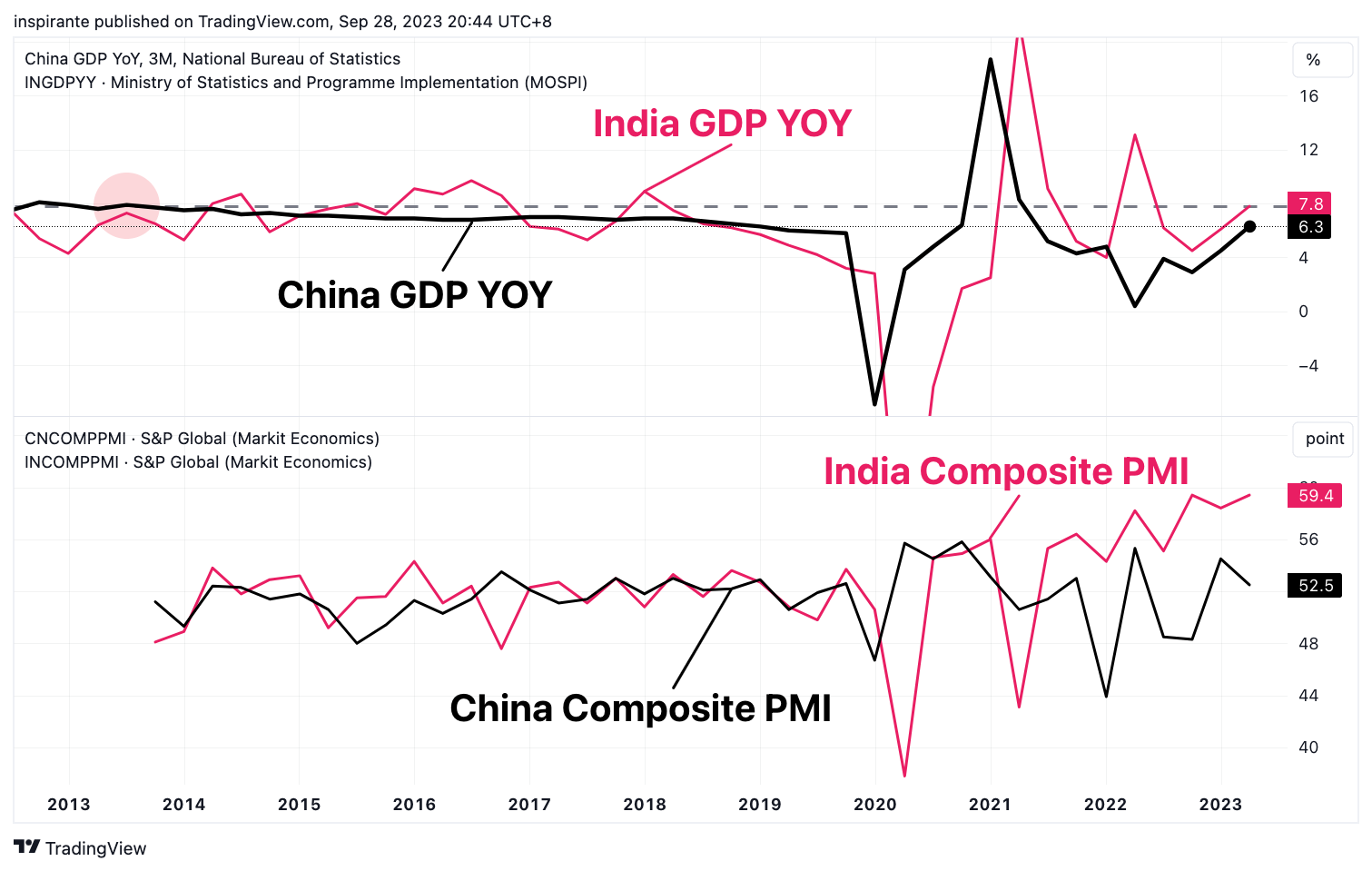

India's impressive year-over-year GDP growth, now standing at 7.8%, is unparalleled when compared to China, especially if you exclude the COVID period. In fact, one has to delve back to 2013 to witness such robust growth from China. Recent economic indicators such as the composite PMIs also suggest India is currently outpacing China.

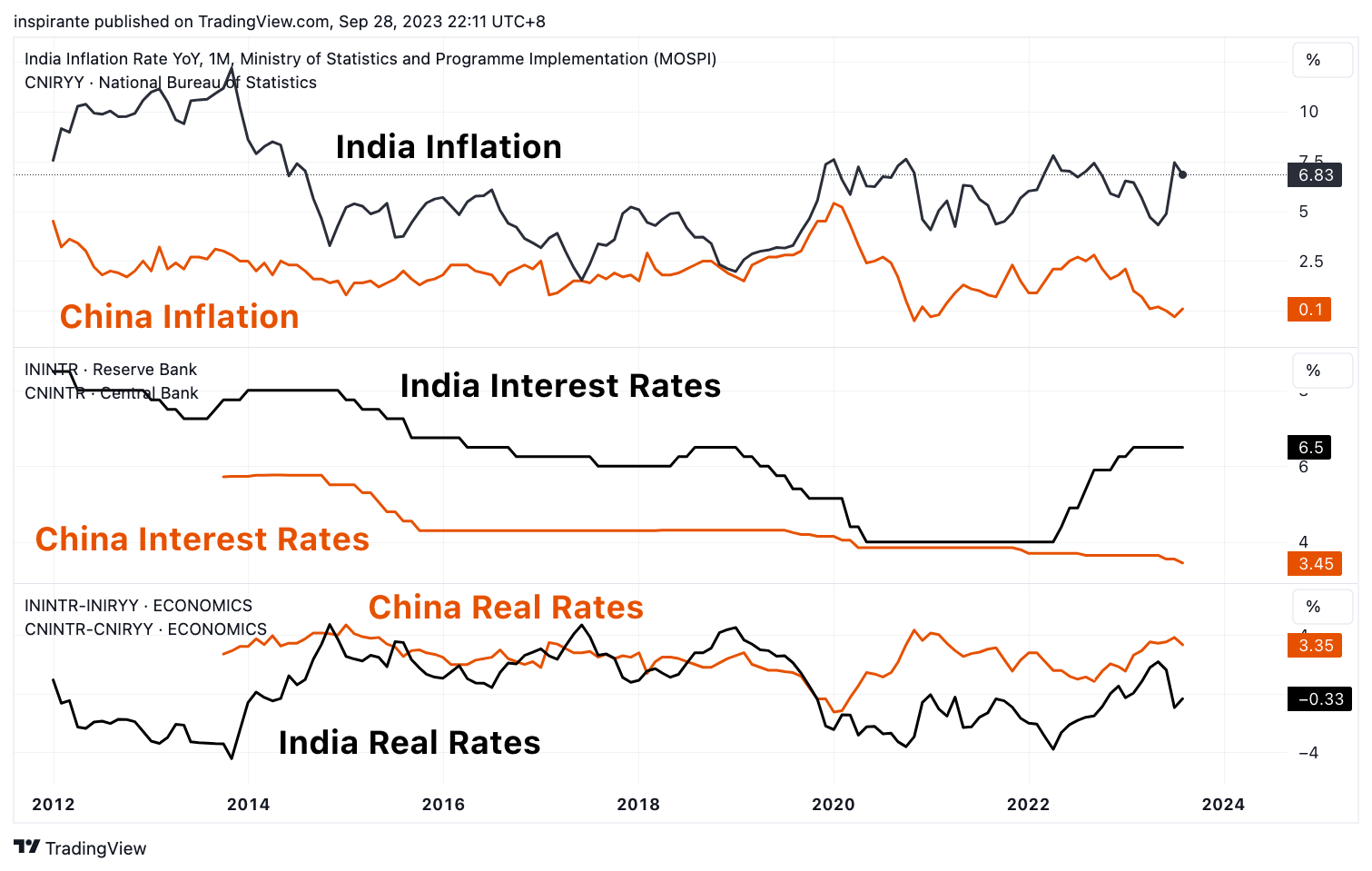

Interestingly, even though India grapples with considerably higher inflation than China, when examining both inflation and prevailing interest rates in tandem, India’s monetary policy appears more supportive. This is evidenced by India's negative real rates, in contrast to China's positive ones.

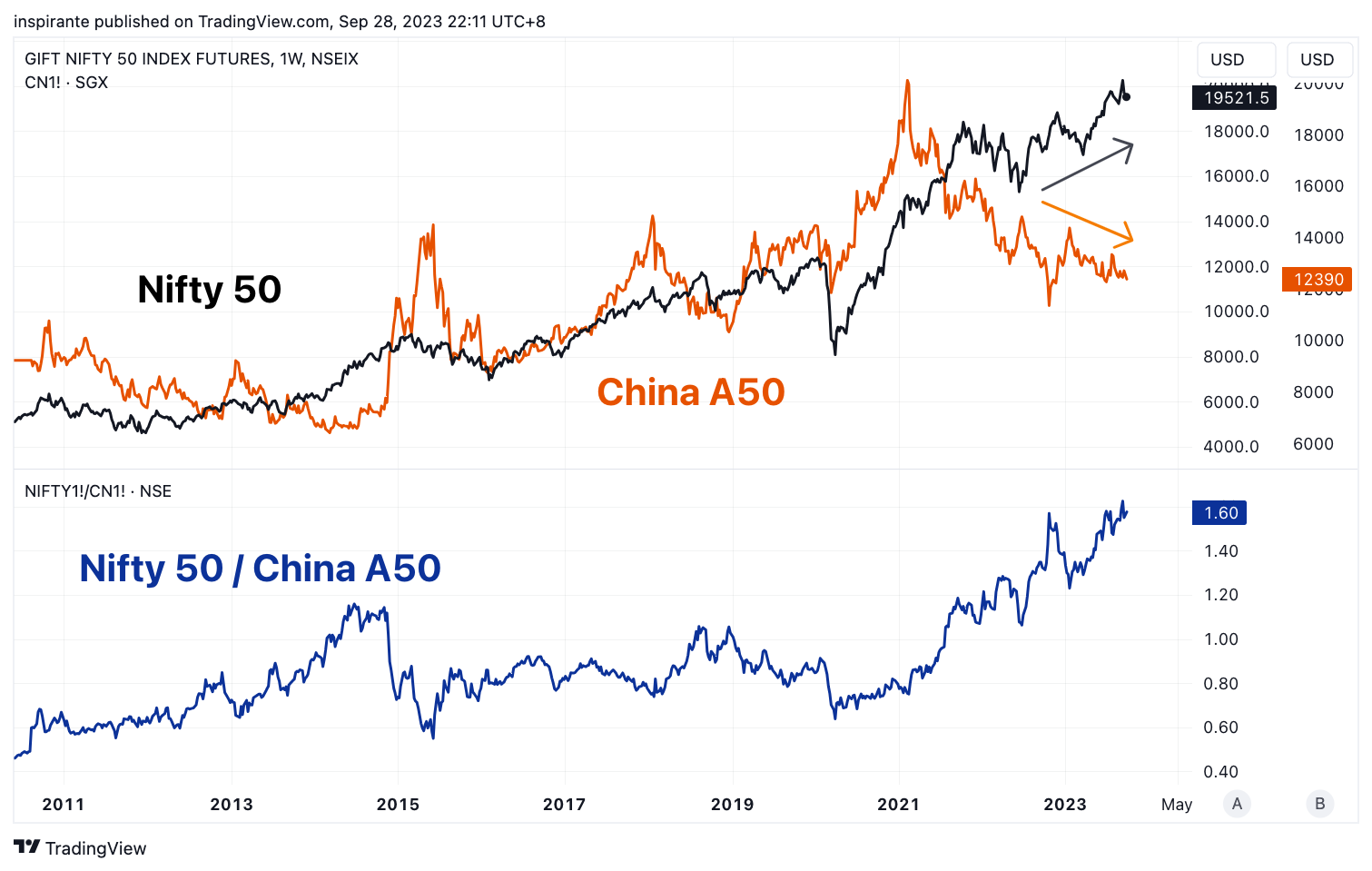

Hence we see some support for Indian equities to outperform. The divergence in economic performance between the two nations is evident in their respective equity markets, with the Nifty 50 and China A50 indices notably parting ways. A clear representation of this trend emerges when observing the ratio of the two indices. This begs the question: Have investors been excessively bearish on China and overly optimistic about India?

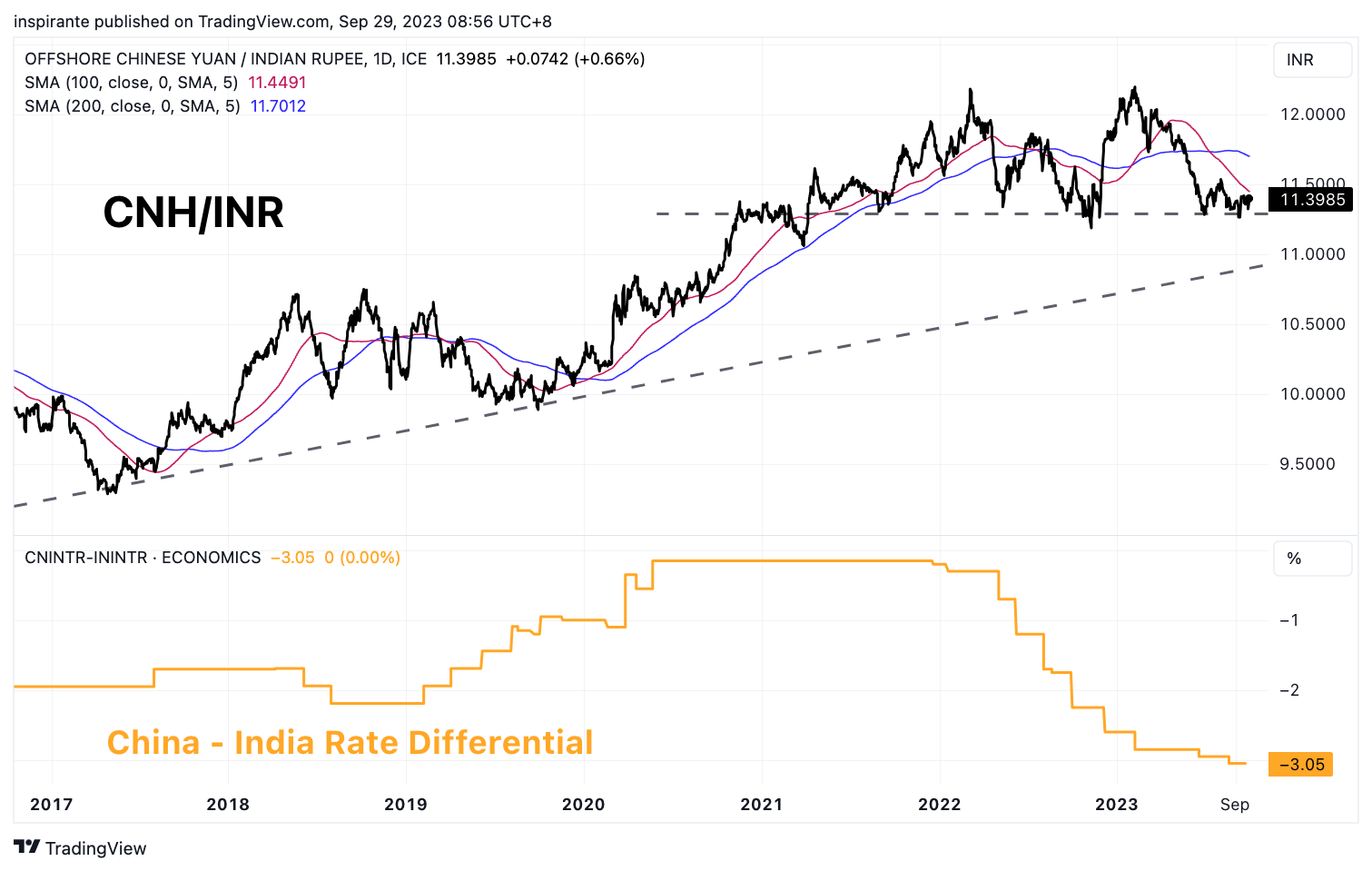

On the topic of India and China, it's hard to overlook the CNH/INR cross trading at a critical support level. The interest rate differential between the two countries has traditionally provided a rough guide for the currency trajectory. With the rate differential now negative, this favours the INR against the CNH.

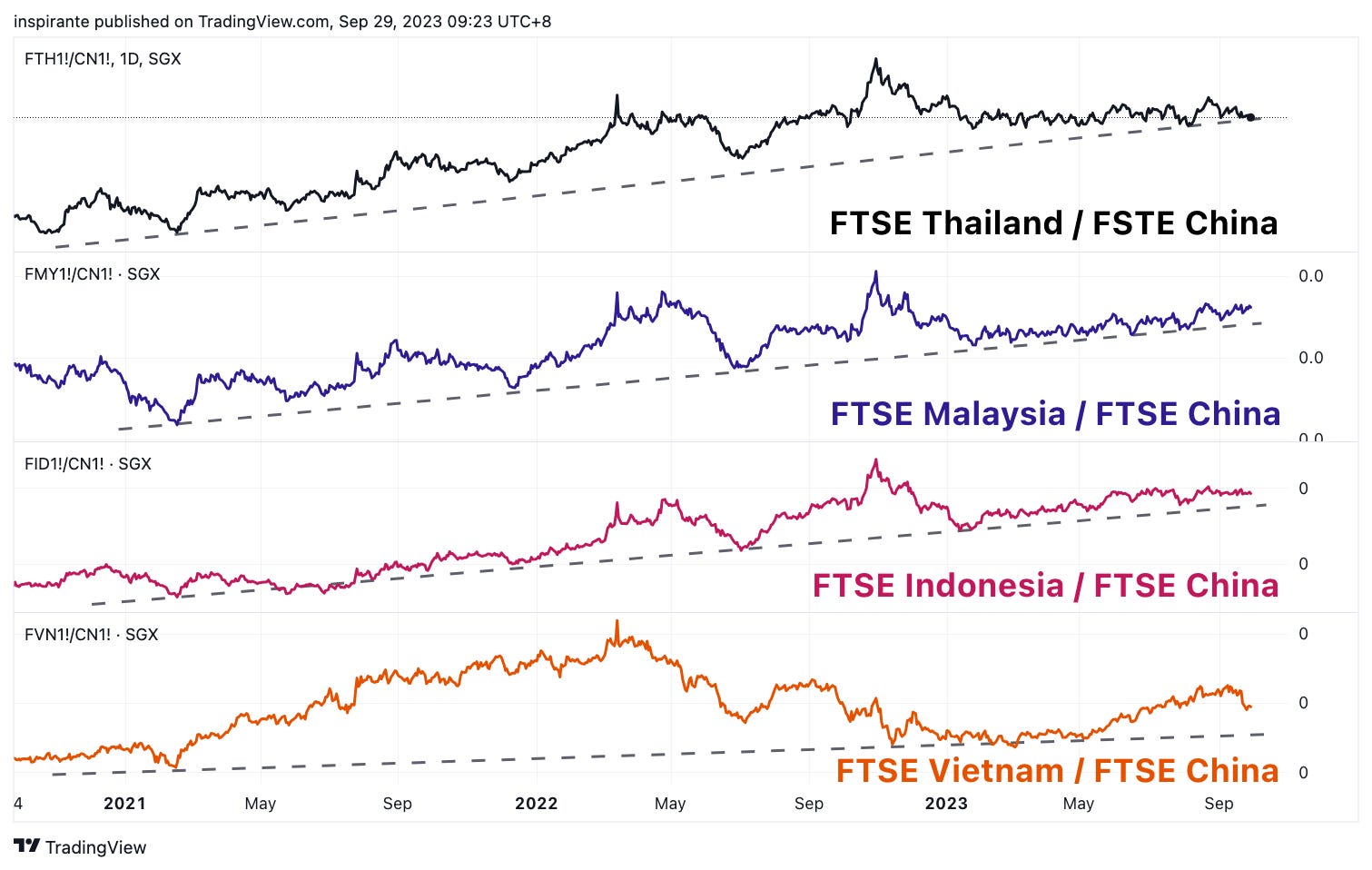

China's waning influence isn't just limited to its relationship with India. A comparative analysis with other Asian emerging markets reveals a consistent upward trend in index ratios since 2021, showing investors tilting preference from China to other emerging markets.

What’s inside our playbook?

While not exactly a new phenomenon, the backdrop of ‘de-sino-fication’ has been playing out not so subtly, evident from anecdotes such as Apple beginning production of iPhone from India, or even as far back as the US-China Trade wars. As global investors grow wary of their investments exposure in China, they confront an essential question: Where next? We believe the answer lies in Asian emerging economies, rich in youthful demographics and a growing middle class. Among these nations, India is uniquely poised to attract attention.

“I think the optimism of India is actually completely justified" – JPMorgan Chase Chairman and CEO, Jamie Dimon

Jamie Dimon’s recent comments on India has sparked interest and kicked up a debate on India as a compelling alternative to China. As the world’s most populous country and the 5th largest in terms of GDP, India's significance is undeniable. But beyond these credentials, its current economic performance is what's turning heads. Boasting a year-on-year GDP growth of 7.8%, one must rewind to China's 2013 metrics—excluding COVID-induced fluctuations—to find a parallel.

Every investment landscape comes with its own set of challenges. For India, its role as the world's third-largest energy importer presents vulnerabilities, especially with global oil prices on an upswing. Such a situation could accelerate inflation, putting pressure on household incomes and possibly dampening consumer spending. But it's not all gloomy for now as India's pivot to Russian oil to meet its demands, combined with a softer-than-expected reading for its September Inflation numbers, points towards a possible peak in its inflation. Still, it's vital to acknowledge the historical volatility of oil prices, influenced significantly by major macro events like OPEC production adjustments or geopolitical unrest. Therefore, while our outlook remains cautiously optimistic, we're keeping a close watch on energy commodity price fluctuations and emerging macroeconomic developments.

The present economic environment, characterized by negative real rates, offers the Reserve Bank of India (RBI) more flexibility to adopt a hawkish monetary policy without excessively impeding growth. Additionally, a hawkish move by the RBI could bolster the Rupee which becomes even more relevant when juxtaposed against the Chinese Yuan, which has been trading weaker. Again, we will closely monitor developments related to the Yuan, especially announcements from the PBOC or the politburo, and adjust accordingly in response to these changes.

On the equities front, the favorable real rates in India are a boon for investors. Historically, low real rates have often correlated with bullish equity markets. And given the current global investment climate, with funds potentially redirecting from China in search of more stable returns, India is poised to capture a significant share of this capital movement. Such an influx could further fuel the Indian market's momentum, making the optimism of India, justified.

Executing the plays

A hypothetical investor can consider the following two trades1:

Case Study 1: Long NSE IFSC Nifty 50 Index Futures (GIN) and Short FTSE China A50 Futures (CN)

We would consider going long the Nifty 50 and short the China A50 using a long position in the NSE IFSC Nifty 50 Index Futures and a short position on the FTSE China A50 Index Futures both listed on the SGX. Expressing a long position on the Nifty 50 Index Futures at the current level of 19632.5, and a short position on the China A50 Index Futures at the current level of 12498 will give us a entry ratio of roughly 1.57. Setting a stop at a ratio of 1.45 and take profit at the ratio of 1.80. Each index point move in the FTSE China A50 Index Futures is 1 USD and each point move in the NSE IFSC Nifty 50 Index Futures is 2 USD.

Case Study 2: Long SGX INR/USD FX Futures (IU) and Long SGX USD/CNH FX Futures (UC)

We would consider taking a short position on the CNH/INR FX pair by taking a long position on the SGX INR/USD FX Futures (IU) and a long position on the SGX USD/CNH FX Futures (UC) to create a synthetic short CNH/INR FX position. A short position at the current level of 11.403, stop at 11.633 and take profit at 10.660 will give us a reasonable risk-to-reward ratio. The contract size for the INR/USD contract is roughly 24,000 USD while the USD/CNH futures contract is 100,000 USD, hence we can roughly hedge four INRUSD futures contracts with one USDCNH futures contract to form the synthetic currency pair.

Original Link: https://www.sgx.com/research-education/market-updates/20230930-derivatives-traders-playbook-capitalizing-india-china

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.

| A guest post by

|