Like a hot knife through butter

Like a hot knife through butter

First published on 2022-05-11

Markets in Focus

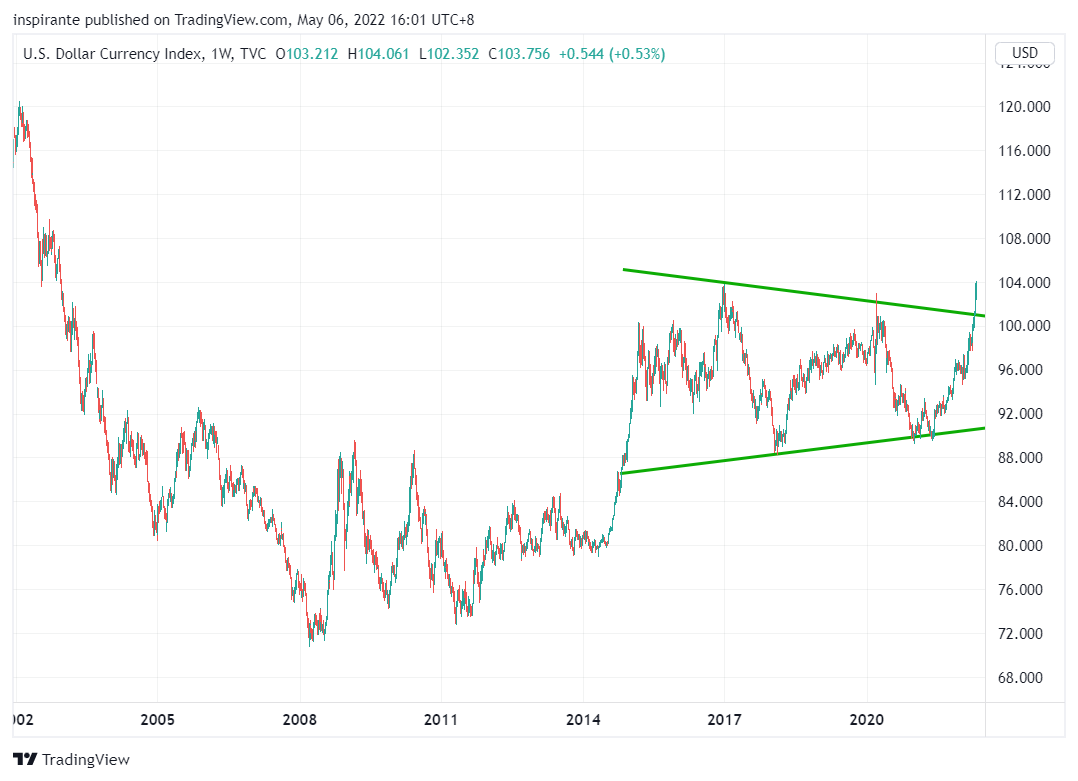

The US Dollar has accelerated its move in the past few weeks, having breached the pandemic high and reaching the highest level in nearly a decade. A strong US Dollar tightens financial conditions meaningfully, and too fast a rise has historically been proven unfriendly to risk assets.

Since we flagged out the potential further weakening of the CNH just two weeks ago, this pair went through critical resistance levels of 6.5, 6.6, and 6.7 like a hot knife through butter. If the policy divergence exacerbates further, we might wonder how soon we could see this pair reach 7.0 and beyond.

The US equity market has been under pressure, especially the small caps and tech stocks. The Russell 2000 Index, after consolidating for three months, once again broke down from the 1900 support level. The next support is at 1700, suggesting the index could still have another 10% to fall.

Copper has failed to break out from the massive ascending triangle. Instead, it has broken down from the support line in the recent risk-off moves. Ascending triangles are typically continuation patterns, but we need to consider the reversal case properly, given central banks’ tightening policies and a very strong US Dollar.

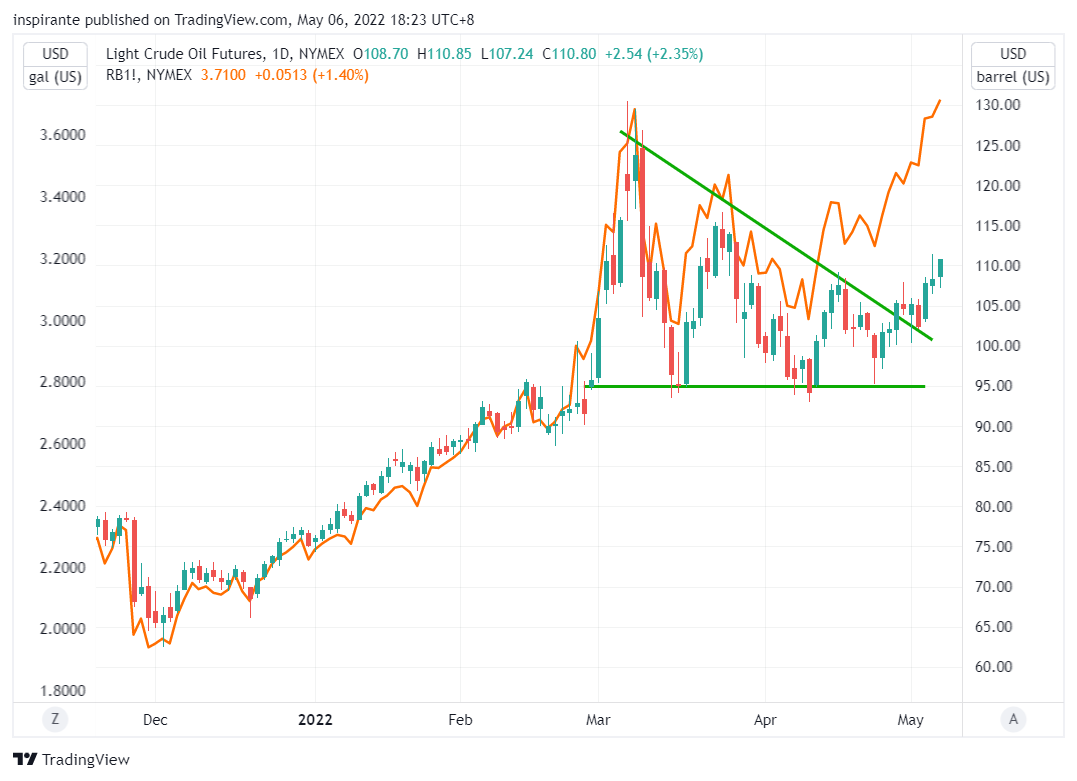

On the other hand, Crude Oil has broken out from the six-week descending triangle, following the RBOB Gasoline breakout, which we have discussed in the previous issue. Despite the headwinds from tighter policies and a strong US dollar, the fundamental energy shortage is the dominant driver of the price actions.

Market Views

The May FOMC meeting concluded with the Fed delivering its first 50bps rate hike since May 2000, exactly 22 years after the peak of the dot-com bubble! More 50bps hikes are still on the table for the next few FOMC meetings. The Fed is determinedly hawkish now.

The market did not take it too kindly. On Thursday, the one-day post-FOMC rebound in the US equity market was brutally erased by relentless selling. For many assets, the central theme of the price actions in the past two weeks has revolved around critical levels being broken furiously, with little pushback. Like a hot knife through butter, indeed.

The speed and magnitude of the US Dollar strengthening should raise a red flag for investors, as it puts considerable pressure on risk assets, especially emerging markets and commodities. Copper is one of them. As one of the essential base metals, copper is closely tied to the economic cycles. Although the global move to Electronic Vehicle (EV) will lead to manifold demand for copper in the next 5-10 years, the tightening of monetary policies and the deliberate cooling of economic activities inevitably suggests downside risk in the short term.

Compared to copper, crude oil has a much more robust bull case even amid tightening monetary policies and a strong US Dollar. People need to use fossil fuels in their daily lives. Many countries are facing severe energy shortages right now. The imminent demand and supply imbalance means crude oil will likely outperform copper on a relative basis even if the entire commodity space experiences further risk-off events.

Finally, being bullish on crude oil and bearish on copper shield investors against volatile US Dollar moves while maintaining their commodity exposure.

How to play the theme out

A hypothetical investor can consider the following trades1:

Case Study 1: Long Micro WTI Crude Oil Future

If the investor were to long the Micro WTI Crude Oil future (MCLM2) at 109 and set the stop below 95, his maximum loss per contract would be (109 - 95) x 100 = 1400 USD. An initial target points to 120 and subsequently 140, resulting in (120 - 109) x 100 = 1100 USD and (150 - 109) x 100 = 4100 USD.

Case Study 2: Short Micro Copper Future

If the investor were to short the Micro Copper future (MHGN2) at 4.27 and set the stop above 4.6, his maximum loss per contract would be (4.6 – 4.27) x 2500 = 825 USD. An initial target points to 4.0 and subsequently 3.5, resulting in (4.27 – 4.0) x 2500 = 675 USD and (4.27 – 3.5) x 2500 = 1925 USD.

Original Link: https://www.cmegroup.com/newsletters/fresh-from-the-trading-room/files/fresh-from-the-trading-room-2022-05-11.pdf

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.

| A guest post by

|