Likely Higher.

Likely Higher.

Yen traders had quite a few interesting sessions the past week. From almost hitting the three-and-a-half decade high around 160 to suffering one of the largest 5-day correction with the currency hitting below 152 at the low. The 14-day RSI also reached levels only ever seen 1 other time/highest in over 7 years. The 5-day vol also spiked to levels rarely seen since 2017.

So what’s driving this move? While it's hard to pinpoint the exact drivers, several factors likely contribute:

Speculative short yen futures positioning reached the second-highest level recorded since the 1980s.

A densely packed economic calendar last week.

Several market holidays in Japan.

Shifting expectations regarding the timeline for rate cuts.

The decline in interest rate differential seems to serve as a good leading indicator for the turn lower in both the USDJPY as well as the Nikkei 225 Index.

Three of the past four decreases in this differential have led to a temporary increase in the USDJPY before a more substantial decline, coinciding with a drop in the Nikkei shortly after as well.

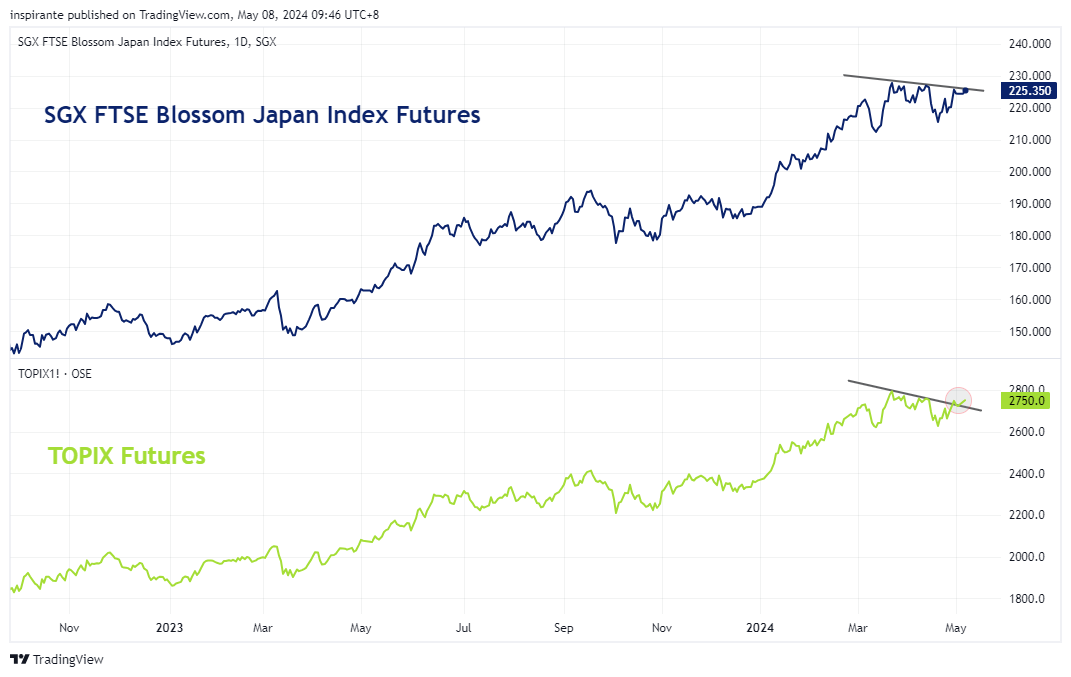

Aside from the Nikkei 225 and the TOPIX Index, another viable route to gain exposure in Japan is through the FTSE Blossom Japan Index.

With similar industry weights and overlapping top 10 components, the FTSE Blossom Japan Index offers an alternative perspective on the Japanese market with a strong preference for ESG.

The correlation between the FTSE Blossom and TOPIX stands at nearly 99%, with the FTSE Blossom Japan Index outperforming since its inception.

Given the close resemblance in price action between the two indices, the current upward breakout in the TOPIX suggests a similar movement in the FTSE Blossom Japan Index as it tests resistance levels.

What’s inside our playbook?

Recently, the yen experienced significant fluctuations, almost reaching a three-and-a-half-decade high, followed by one of the largest corrections in recent years. The 14-day Relative Strength Index (RSI) soared to levels seen only once in the past seven years, while the 5-day volatility reached a peak not observed since 2017. These movements, reflecting underlying market tensions and speculations, were influenced by factors such as speculative positioning according to the COT report, key economic announcements (including the FOMC meeting and unemployment data released last week), several market holidays in Japan and speculations of a MOF intervention.

While short-term volatility can be exhilarating, especially with potential MOF intervention looming, it poses significant risks. It's challenging to predict when authorities might step in. Thus, a more stable, long-term approach to understanding the potential path for the USDJPY involves examining the interest rate differential between the US and Japan.

From longer-term perspective, we think the US-Japan interest rate differential provides a much better framework for understanding the currency path. As seen in Figure 2, when viewed together, the peak in the interest rate differential between the 2 countries provides a good marker for the turn lower in the USDJPY. Amongst the past 4 instances since 1988 when the rate differential declined, 3 of which had the USDJPY initially gaining before a substantial drop, while the most recent episode had the USDJPY just trading lower without the initial run up. Episodes of such moves could be attributed to the unwinding of the yen carry trade where as the yen appreciates, carry traders may lock in profits by selling their foreign investments and repurchasing yen to repay loans, thereby driving the yen even higher and prompting further unwinding.

Interestingly when we overlay the interest rate differential on the Nikkei 225 Index, as a proxy for the Japanese market in Figure 3, we also observe that the peaks in the interest rate differentials also generally lead the peaks in the equity index. In four of the past reductions in rate differential, we see the equity index tumbling shortly after the interest rate differential has declined sharply. This correlation may be because as the rate differential narrows, the yen strengthens, as seen in Figure 2, diminishing the export competitiveness of export-reliant Japanese companies, which are heavily represented in the index, thus hurting the index.

The critical question then is: where is the rate differential headed, and has it peaked?

On the Japan front, the March rate hike by the Bank of Japan (BOJ) signaled the end of the negative interest rate regime. While this might seem like the beginning of a new chapter for the BOJ, inflation—or rather, the lack thereof—remains a concern. Core inflation, as measured by YoY Japan Nationwide CPI excluding Fresh Food and Energy, has shown signs of slowing. As a country that imports nearly 90% of its energy needs, the clear correlation between crude oil prices and Japan’s CPI is evident, with fluctuations in oil prices closely leading changes in the CPI. Given that crude oil prices are currently rangebound, their next movement will likely illuminate the potential path for Japanese inflation. Additionally, record-high debt to GDP levels might constrain the BOJ's ability to raise rates further, to avoid exacerbating the government's budget deficit due to increased financing costs.

On the US front, persistent inflation brings back memories of the 1970s double peak inflation with the current YOY inflation chart lining up nicely with the period of the 1970s. Financial conditions are still relatively loose and the the S&P500 is still close to all-time highs. Alongside this, the streak of relatively strong nonfarm payrolls numbers as well as a relatively low unemployment rate backs the view that the US economy is still running strong, cutting too early might just result in a resurgent inflation like in the 1970s. However, as employment numbers came out weaker than expected last Friday, expectations of the timeline of cuts seem to be pushed forward again as seen from, the change in the implied fed fund rate probabilities as well as the S&P500 staging another rally on Friday.

While there are expectations for the Federal Reserve to cut rates, we believe they will tread cautiously, as will the BOJ before its next rate hike, considering the potential impacts on Japan's debt-heavy economy. Consequently, we anticipate some room for the USDJPY to trade higher as we have not yet seen the steep rate cuts that typically precede major declines in the currency.

If the yen continues to weaken, this would bode well for Japanese indices, as a weaker yen enhances the competitiveness of Japanese exports, thereby supporting indices heavily weighted towards exporters. Furthermore, a weak yen could positively impact earnings when repatriated back to Japan. Thus favoring equities if this scenario plays out.

Amongst the Japanese Indices, we think the FTSE Blossom Japan Index presents the most opportunities as its price action looks poised for a breakout higher given its longstanding high correlation with the TOPIX index and the fact that the Topix has recently broken out higher as seen in Figure 6. Additionally, the FTSE Blossom Japan Index has a proven outperformance since its inception versus the other Japanese Indices, with the cherry on top of being overweight on the ESG factor.

The above model provides a framework for reaction when the sustained decline in rate differential begins, but for now, we think there is room higher, for both the USDJPY and Japanese Index.

Executing the plays

A hypothetical investor can consider the following two trade1:

Case Study 1: Long SGX USDJPY (Standard) FX Futures (UY)

We would consider going long the USDJPY using a long position on the SGX USDJPY (Standard) FX Futures (UY) for the following two reasons;

We do not yet see a catalyst that might cause the rate differential close quickly

Even if it does, past episodes show that the USDJPY tends to first rise before collapsing

Keeping in mind the volatile nature of the currency move during this period, we can express a long position at the current level of 155.26, stop at 150, and take profit of 165 will give a reasonable risk-reward. Each 0.005 move in the UY contract is for 500 Yen.

Case Study 2: Long SGX FTSE Blossom Japan Index Futures (EJP)

The potential for the yen to continue weakening will benefit the Japanese Indexes, amongst which the FTSE Blossom Japan Index is the outperformer. Given how similar the FTSE Blossom Japan Index and TOPIX index are, in terms of component weights as well as correlation of the index prices, the recent technical break higher on the Topix, is likely to follow suit on the FTSE Blossom Japan Index. As such we will consider going long the SGX FTSE Blossom Japan Index Futures at the current level of 225.35, stop at 217, and take profit at 240, each 0.025 move is 1250 JPY.

Original Link: https://www.sgx.com/research-education/market-updates/20240508-derivatives-traders-playbook-likely-higher

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.