Oversold and Overbought

First published on 2024-04-11

Iron Ore is once again trading near its long-term support, maintaining its status as a crucial proxy for the Chinese market, as we have previously established in our last piece covering the commodity.

What’s different this time, since our last coverage of Iron Ore, is its divergence from the FTSE China A50 Index. The two, generally closely related, have recently diverged. Using the 50-day correlation as a reference, the current regime of divergence is among the more extended and extreme ones observed over the past decade. The mean-reverting nature of their correlation, suggests this period of divergence will likely end, perhaps with Iron Ore rebounding from its current resistance and a sustained recovery in China after a prolonged sell-off.

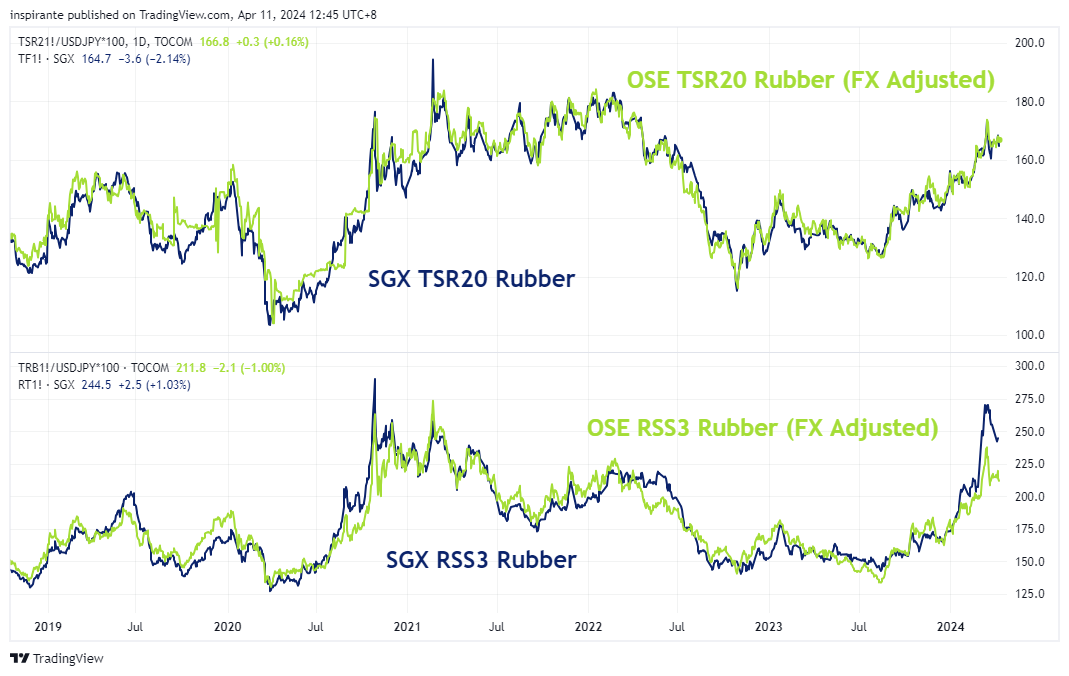

Rubber, another commodity that China leads in terms of consumption, is pivotal. As the world’s top producer of rubber-related products, China also ranks first in imports of rubber types such as Ribbed Smoked Sheets (RSS) and Technically Specified Natural (TSR) Rubber.

As both rubber types are used in similar industries, their prices are interconnected; as depicted in Figure 3. This interconnection is primarily due to both types of rubber being derived from the latex of the Hevea Brasiliensis tree and, interestingly, they maintain a relatively defined spread, albeit with some exceptions.

Rubber as a commodity is unique given that similar rubber futures are traded across various exchanges, including Osaka, Thailand, and China. SGX provides the pricing benchmark for the physical rubber industry globally and is the preferred venue for TSR Rubber in terms of liquidity and open interest.

The availability of similar types of rubber listed on various exchanges allows for clear price discovery. Adjusting for currency, the SGX and OSE rubber contracts become tightly related. This makes sense given the various similarities of the futures contract specification, e.g. the contract size, similar deliverable countries and settlement basis. However, periods of differences still exist, perhaps due to varied liquidity, market hours, currency differences and investor preferences.

The difference in quote currency between SGX Rubber Futures (USD) and OSE Rubber Futures (JPY) introduces an additional perspective from which to compare the two rubber contracts: deriving the implied USDJPY exchange rate. Here, the implied FX rate aligns closely with the FX Futures, though periods of variation do occur.

What’s inside our playbook?

This month’s piece reckons a look at commodities as we delve deeper into the dynamics of Iron Ore and its pivotal relationship with the Chinese market. As previously established in our piece last July, given the country's significant consumption as part of its vast industrial sector, Iron Ore has long been recognized as a critical proxy for gauging the economic pulse of China. Typically, the movement of Iron Ore prices and the FTSE China A50 Index are closely intertwined, reflecting the direct impact of China's economic health on the demand for this industrial metal. However, recent observations reveal a notable divergence between the two, marking a departure from their usually parallel paths. This deviation is particularly striking as we examine the 50-day correlation, finding ourselves in one of the most extended periods of divergence observed in the last decade.

Alongside this, Iron Ore is once again trading near its decade-long support level, after a notable rally from July to December 2023, recent price correction in the first quarter has brought prices back to the decade-long support level. The weekly RSI for Iron Ore is also nearing the oversold level, which has generally marked the major bottoms for the commodity.

This unusual separation suggests an interesting phase, where the mean-reverting nature of the correlation between Iron Ore prices and the FTSE China A50 Index seems to have overstretched, alongside the generally supportive price action for Iron Ore hints at higher Iron Ore prices.

Turning our attention to rubber, another commodity where China's influence is paramount due to its position as the top consumer and producer of rubber-related products, we explore the nuances of TSR20 and RSS3 rubber futures. Both these rubber types, derived from the Latex of the Hevea Brasiliensis tree, are essential for various industrial applications. With tire production counting as the largest consumer of rubber. The differences in prices of TSR20 and RSS3 futures can also be largely attributed to labor cost, with RSS3 rubber production being more labor intensive.

The existence of similar futures contracts for rubber across different exchanges opens up unique arbitrage and strategy opportunities. For instance, the more liquid RSS3 contract on the Osaka Exchange (OSE) can help indicate when the SGX-listed TSR20/RSS3 spread might be trading at a premium as seen in Figure 6. Traders can capitalize on this by selling the spread on SGX as seen in Figure 4, leveraging the liquidity and open interest discrepancies between exchanges. However, it has to also be noted that, while lower in volume, the RSS3 Rubber on SGX is still the preferred benchmark.

Alternatively, a simple arbitrage can also be formed between the SGX TSR20 Rubber as well as the INE TSR20, in which the products are closer substitutes, which stands to reason for a closer correlation between as well as a tighter price movement. The main differences here are the currency denomination, price quotation and contract size, all of which can be adjusted and hedged allowing for a ‘pure’ arbitrage; though it is good to note the difference in the respective delivery option as well. The INE TSR20 Rubber Futures is quoted as CNY/MT for 10 MT with warehouse delivery, while the SGX TSR20 Rubber Futures is quoted as US cents/Kg for 5 MT with Free-on-Board delivery.

If we adjust the SGX TSR20 rubber to Dollar/MT and then apply the prevailing USDCNY exchange rate, we get;

Here we see the FX adjusted price difference of the two products, with periods of deviation that one can capitalise on.

Another unique way to look at Rubber is to use the fact that the TSR20 contracts listed on both SGX and OSE are quoted in different currencies but have a very similar contract specification and deliverable grade. Hence, we can use both contracts to calculate the implied USDJPY exchange rate. Observing the correlation and disparities between these contracts and the actual USDJPY futures on SGX can uncover potential discrepancies ripe for trading strategies. This analytical approach not only allows for direct commodity trading strategies but also opens the door to more sophisticated forex plays based on commodity futures pricing.

Executing the plays

A hypothetical investor can consider the following two trades1:

Case Study 1: Long SGX TSI Iron Ore CFR China (62% Fe Fines) Index Futures (FEF)

We would consider taking a long position on Iron Ore using the SGX Generic 2nd TSI Iron Ore CFR China (62% Fe Fines) Index Futures (FEF) contracts given the dislocation of the commodity with its historical relation with the China A50 Index as well as the support price action. From the current level of 106.7, we will take a risk-measured stop at 92, and take profit at 126, each 0.05 move is equal to 5 USD.

Case Study 2: Short SGX SICOM RSS3 Futures (RT), Long SGX SICOM TSR20 Futures (TF)

Using the OSE Rubber prices as a reference, the RSS Rubber on SGX seems to be trading on the high. This alongside the overextend spread between the RSS3 Rubber and TSR20 Rubber on SGX leads us to consider taking a short position on the Rubber spread. This can be set up by taking a short position on the SGX SICOM RSS3 Futures (RT) and a long position on the SGX SICOM TSR20 Futures (TF). Using the range in Figure 4 assuming the spread normalizes, we would set the take profit at a conservative 40 level and stop at 110 to provide an attractive risk-reward, each 0.1 move is 5 USD.

Original Link: https://www.sgx.com/research-education/market-updates/20240411-derivatives-traders-playbook-oversold-and-overbought

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.