The effect of rate cuts

Written on 2024-09-30

The US Federal Reserve has made its move, not gently but with a decisive 50 bps cut. The effect? A broad rally in equities.

Chasing the rally may seem tempting, but first, let's look back at how previous rate cuts have affected the Singapore Index.

Rate cuts typically impact different sectors in varying ways, with financials often the most sensitive as their income streams are closely tied to interest rates.

With financials making up nearly 55% of the MSCI Singapore Index, it is important to take a closer look at the index and its components following this major macroeconomic shift.

The effect of the last three rate cuts on Singapore’s three largest local banks—DBS, UOB, and OCBC—has been clear. While other macroeconomic factors were also in play during those periods, it is undeniable that banks generally suffer from lower interest rates due to compressed net interest margins.

As we highlighted in May, the ratio of the two indices had been trading in a well-defined upward trend until recently.

Delving into the individual indices, it’s interesting to note that the ratio broke lower, mainly due to the MSCI Singapore Index rallying more than the FTSE Taiwan Index.

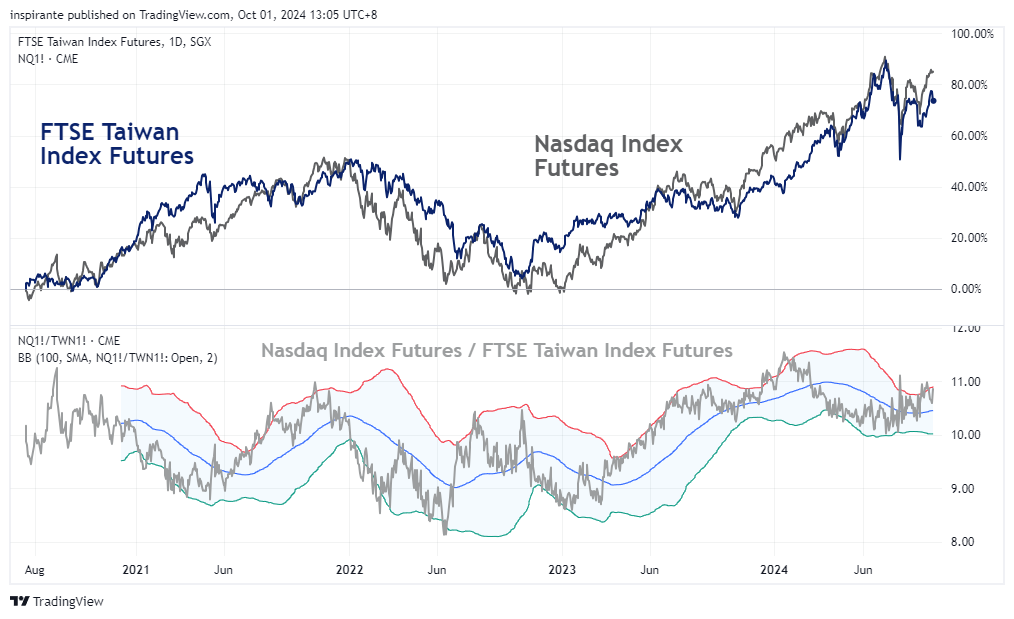

Since 2020, the FTSE Taiwan Index Futures have followed Nasdaq Index Futures closely. The correlation between these two indices is driven by their similar weighting towards semiconductors and technology, resulting in highly comparable movements.

What’s inside our playbook?

With major central banks, including the Federal Reserve and the Bank of Japan, having announced their policy decisions, global equity markets are feeling the ripple effects. The recent 50 bps cut by the US Federal Reserve triggered a broad rally in equities, but it’s essential to look at how past rate cuts have historically impacted different sectors, especially in Asia.

Financials tend to be highly sensitive to interest rate changes as their revenue streams are tied to interest-related income. The MSCI Singapore Index, with a 55% allocation to financials, is particularly vulnerable to rate changes. As seen in previous cycles, rate cuts have nuanced impacts on various components of the index, especially the largest local banks—DBS, UOB, and OCBC (Figure 3). These banks typically experience compressed net interest margins in a rate-cutting environment, which reduces profitability and, in turn, pressures the MSCI Singapore Index. Given that we are entering another rate-cutting environment, the broader impact on the MSCI Singapore Index and its financial components must be considered.

Interestingly, despite its heavy financial sector exposure, the MSCI Singapore Index has yet to show signs of strain and has outperformed when compared to the FTSE Taiwan Index, a contrast to historical behavior (Figure 4).

This divergence presents a potential trade opportunity in the form of a long FTSE Taiwan/short MSCI Singapore position. As shown in Figure 4, the ratio of FTSE Taiwan RIC Capped Index Futures to MSCI Singapore Index Futures has been trending upward over the past two years, reflecting Taiwan's outperformance over Singapore. This trend is likely to continue as Taiwan’s technology sector benefits from global demand, while Singapore’s financial sector faces challenges from rate cuts.

Taiwan’s strength is largely attributed to its semiconductor and technology sectors, which have benefited from global demand for chips and AI-related products. The correlation between the FTSE Taiwan Index and the Nasdaq Index has strengthened over the past few years due to the AI and semiconductor boom, bringing the two indices into closer alignment (Figure 6). Notably the FTSE Taiwan Index Futures T+1 Volume has also grown to 38% of its daily volume as it gains more traction during the European and US trading hours.

This relationship also manifests in a mean-reverting ratio, which trades within a defined range. The upcoming US election could spur volatility in the Nasdaq 100 Index, and different electoral outcomes could sway the index's movement. Such volatility may present attractive opportunities for mean-reversion trades as short-term swings in the Nasdaq 100 could push the ratio outside its usual trading range.

Executing the plays

A hypothetical investor can consider the following two trade1:

Case Study 1: Long SGX FTSE Taiwan Index Futures (TWN), Short SGX MSCI Singapore Index Futures (SGP)

We would consider going long the SGX FTSE Taiwan Index Futures and shorting the SGX MSCI Singapore Index Futures, based on;

The sensitivity of the MSCI Singapore Index to interest rate cuts.

The momentum in the AI/Chips sector, where the FTSE Taiwan Index has significant exposure.

Hence we can express a long position on the SGX FTSE Taiwan Index Futures (TWN) at the current level of 1870 and a short position on the SGX MSCI Singapore Index Futures at the current level of 341.25, which should give us a ratio entry level of 5.47.

The notional value of the TWN contract in USD is:

1,870 x 40 USD per Point = 74,800 USD (~ 97,240 SGD after conversion)

For the SGP contract, the notional value in SGD is:

341.25 x 100 per Point = 34,125 SGD

To match the notional value of both contracts, a 1 (TWN) : 3 (SGP) ratio would be used. Setting the stop at 5.20 and the take profit at 6 could bring us a hypothetical maximum loss of 0.27 spread points and profit of 0.53 spread points. Each 1-point move in the TWN Futures is 40 USD while a 1-point move in SGP Futures is 100 SGD.

Case Study 2: CME Micro E-mini Nasdaq-100 Index Futures (MNQ), SGX FTSE Taiwan Index Futures (TWN)

As shown in Figure 6, the mean-reverting nature of the spread suggests a trading opportunity. We would monitor election volatility and trade the spread between the two indices if the ratio trades outside the 2 standard deviation Bollinger Band.

At the current price of 1,870 for TWN and 20,260 for MNQ, the notional value in USD for TWN is:

1,870 x 40 USD per Point = 74,800 USD

While the notional value for MNQ in USD will be:

20,256 x 2 USD per Point = 40,512 USD

To balance the notional exposure, we would trade 2 MNQ contracts for every 1 TWN contract, resulting in a net exposure of:

2 x 40,512 = 81,024 USD

81,024 USD (2 MNQ) – 74,800 USD (TWN) = 6,224 USD

If the spread trades above the upper band, we can sell 2 MNQ and buy 1 TWN, and vice versa.

Each 1-point move in the MNQ Futures is equivalent to 2 USD, while each 1-point move in the TWN Futures is 40 USD.

Original Link: https://www.sgx.com/research-education/market-updates/20240930-derivatives-traders-playbook-effect-rate-cuts

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.