The Iron Ore – Copper Dynamic

The Iron Ore – Copper Dynamic

First published on 2023-08-08

Flipping through the markets

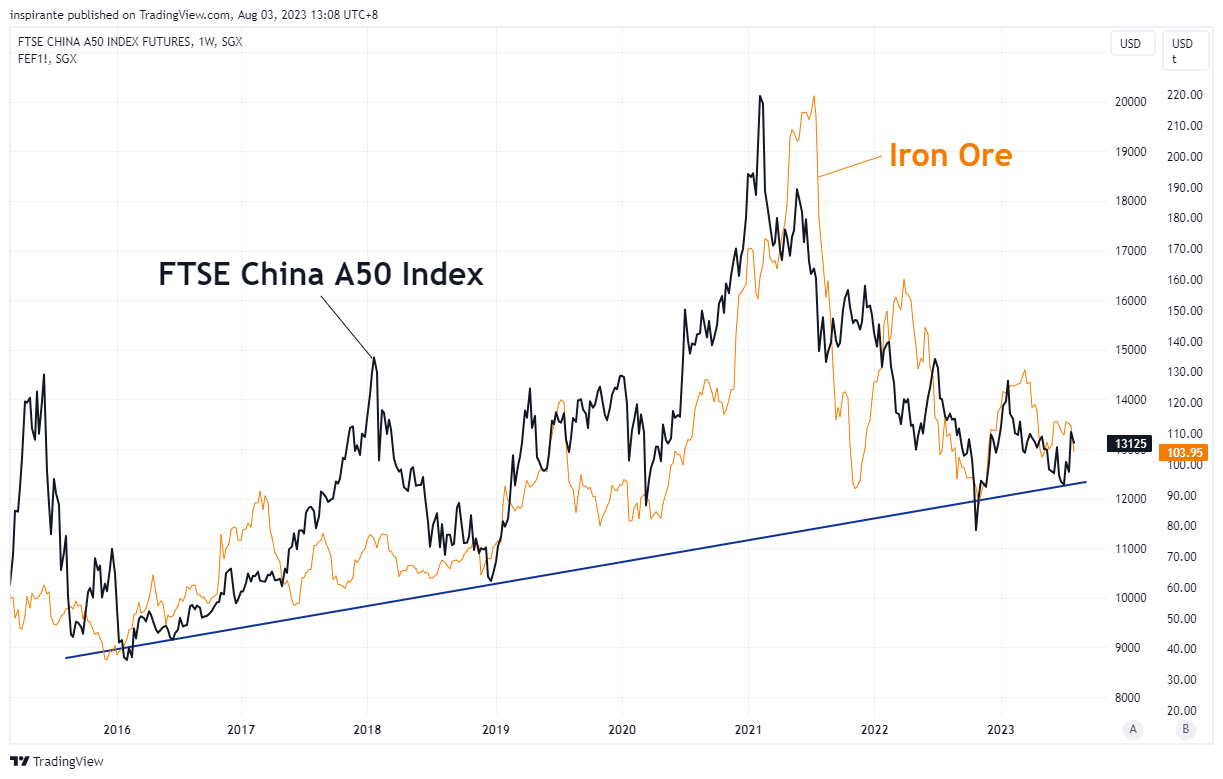

Iron Ore has maintained a 13-year uptrend, with multiple attempts at breaking lower repeatedly thwarted. With prices now teetering on the trendline, there seems to be some support for Iron Ore here.

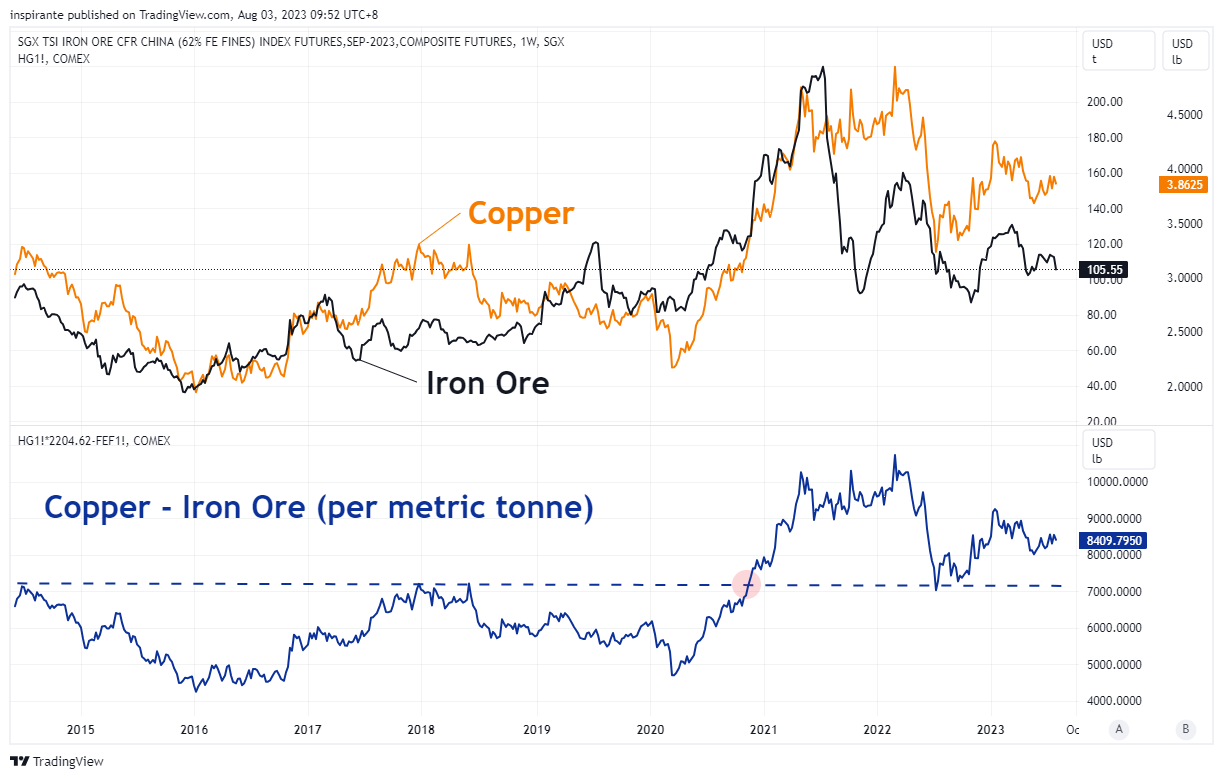

Iron Ore has generally moved in sync with Copper, and both are considered leading indicators of industrial and economic cycles, as they are crucial raw materials for many industries. Recently, Iron Ore has underperformed Copper, which becomes apparent when we compare them on a per metric tonne basis. Could this signal potential support for Iron Ore to catch up?

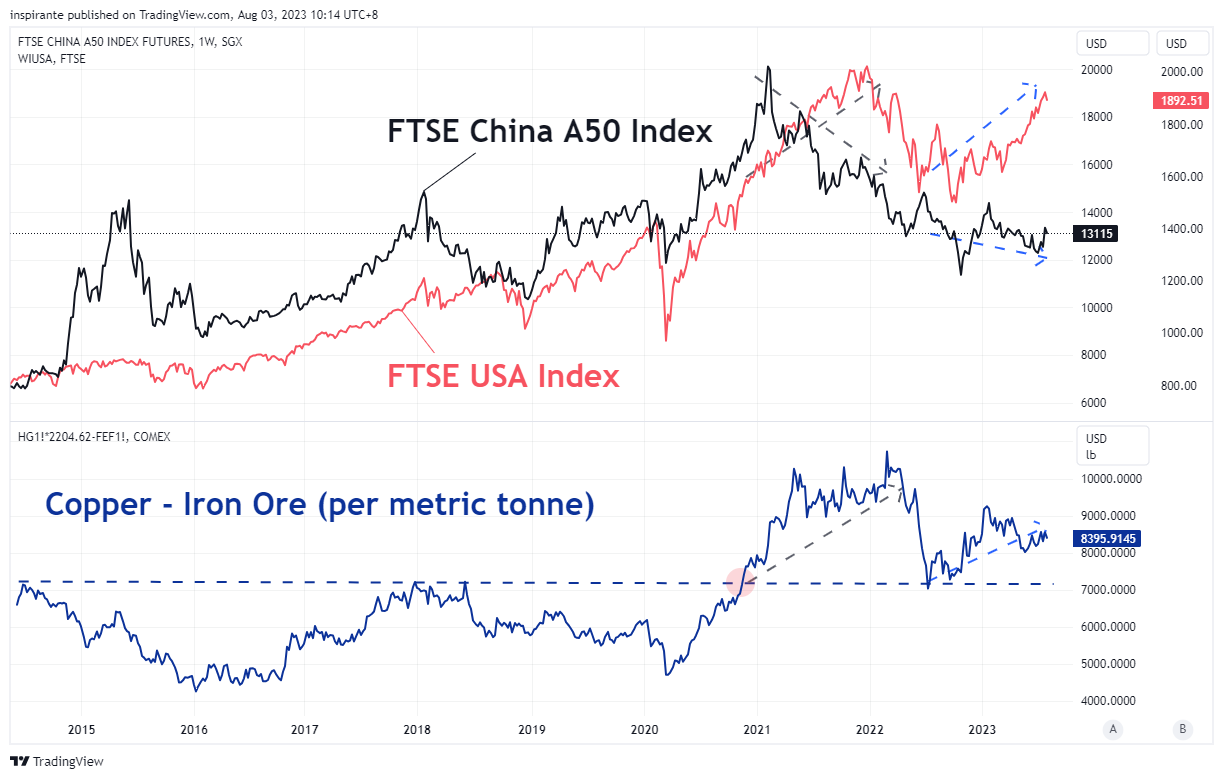

The premium of Copper over Iron Ore becomes interesting as we perceive Iron Ore as a proxy for China and Copper as a proxy for the Western world, especially the USA. Thus, a rising Copper/Iron Ore premium could be interpreted as a tilt towards the USA versus China.

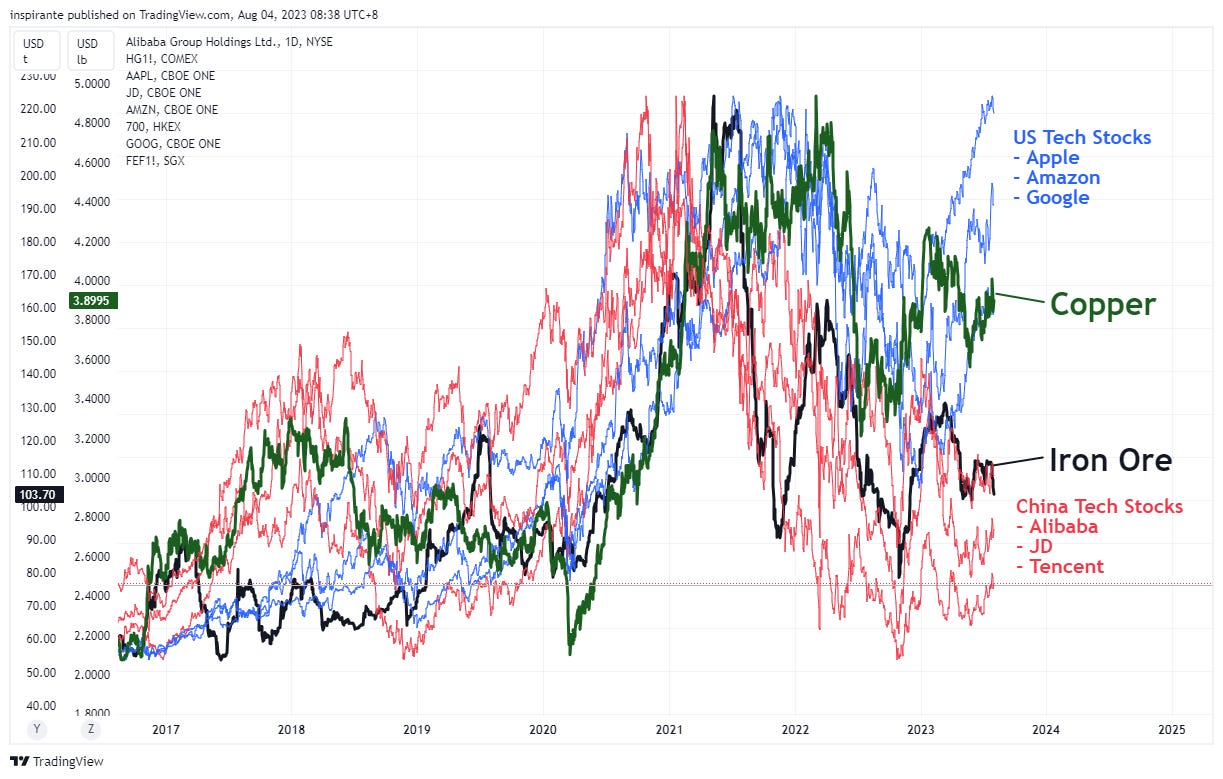

To further illustrate this, we can take a look at the top US & China tech stocks against Copper and Iron Ore. Here, we see the China tech stocks underperforming the US tech stocks in line with iron ore’s underperformance against copper.

This leads us to examine China. The FTSE China A50 Index trades in parallel with Iron Ore, reinforcing our earlier idea that Iron Ore is a reliable proxy for the Chinese market. The index currently sits on an uptrend that has lasted eight years, with prices close to the trend support.

We last highlighted the Vietnam 30 Index in our May edition when the index just broke out of a symmetrical triangle. The index continues its bullish surge upwards and now trades 15% higher from the breakout point. However, this impressive run now faces some resistance near the significant psychological level of 2000.

What’s inside our playbook?

"Iron ore is intimately linked to Chinese economic cycles... stimulus and infrastructure developments and perhaps could be on a par or even better than copper as a global economic macro proxy going forward," - Jin Yu Cheong, director of commodities, Singapore Exchange SGX

This comment comes timely now as Iron Ore and the Chinese Equities markets find themselves at critical junctures.

The current positioning of Iron Ore and the Chinese equities markets underscores a crucial interplay between these commodities and the overall economic picture. The potential for Iron Ore to bounce back from its recent underperformance further hints at an upcoming economic upswing. But what could be driving this potential upswing in the Chinese economy?

We see a few key changes happening in the Chinese economy that could tilt the fortunes ahead.

Firstly, In late July, a politburo meeting expressed clear support for capital markets, indicating that more comprehensive easing measures may be on the horizon. This sentiment aligns with the increased foreign buying seen in mainland Chinese equities in July, suggesting a renewed international confidence in the Chinese market.

Secondly, China stands out as one of the few economies currently implementing an easing policy, with the People’s Bank of China cutting its benchmark lending rates in June and further easing expected to follow.

Although broad economic indicators signal a degree of fragility, as highlighted in last month's edition, the robust support from the central bank and government cannot be underestimated. Considering this, and juxtaposing it against the somewhat inflated performance of the US indexes strengthens the case for a more China-favoured perspective in our view.

Executing the plays

A hypothetical investor can consider the following two trades1:

Case Study 1: Long FTSE China A50 Index Futures (CN)

We would consider going long on the China A50 index given the government and central bank support in China. This view can be expressed using the FTSE China A50 Index Futures (CN) contracts, where each 1-point move is equal to 1 USD. From the current level of 13122, a stop slightly below the trend support at 12150 and take profit at 14250.

Case Study 2: Long SGX TSI Iron Ore CFR China Futures (FEF)

We would consider taking a long position on Iron Ore using the SGX TSI Iron Ore CFR China Futures (FEF) contracts, where each 0.05 move is equal to 5 USD. From the current level of 104.2, we will take a risk-measured stop at 98, slightly below a previous level of support, and take profit at 120.

Original Link: https://www.sgx.com/research-education/market-updates/20230731-sgx-traders-playbook-iron-ore-copper-dynamic

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.

| A guest post by

|