Two lines in the sand

Two lines in the sand

First published on 2023-10-30

Flipping through the markets

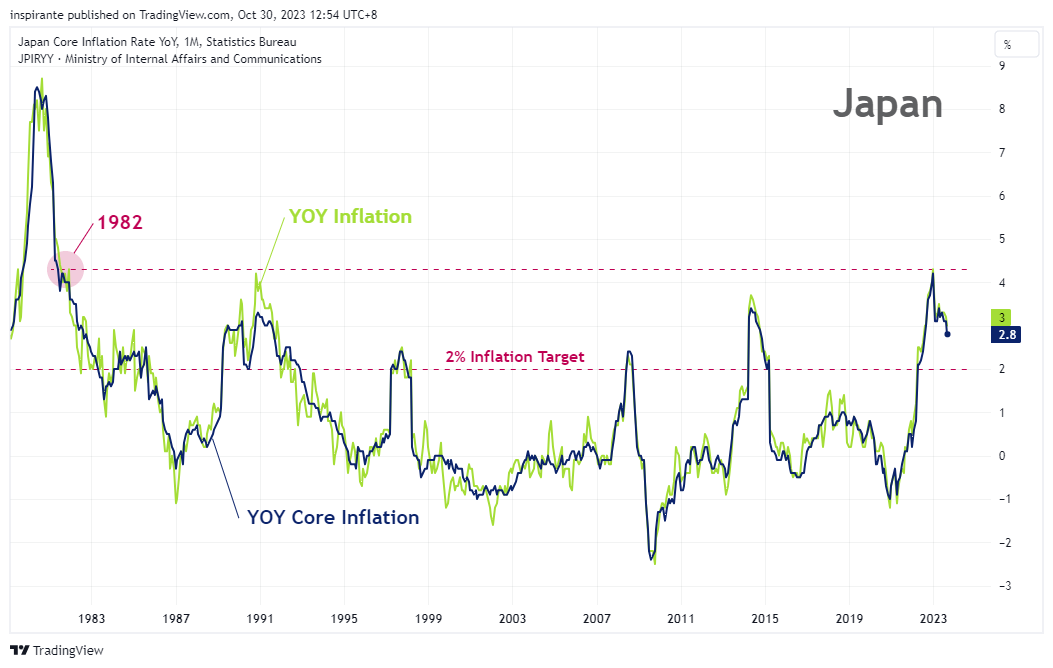

Japan has struggled to counteract the persistent deflationary trend that started in the 1990s. Compared to other economies, Japan’s long-term average inflation rate remains lower and less reactive, evident from its closely intertwined core and headline inflation rates. However, recent spikes in inflation appear more enduring than earlier instances.

In fact, the current inflationary cycle peaked at 4.3% for headline inflation, a level not observed since 1982. Core inflation has surpassed the Bank of Japan (BoJ) target rate of 2%. Notably, the ongoing 17-month inflationary surge is the second-longest period above the 2% target since the 1990s. Recent inflation data surpassed expectations, prompting concerns about Japan's inflation scenario.

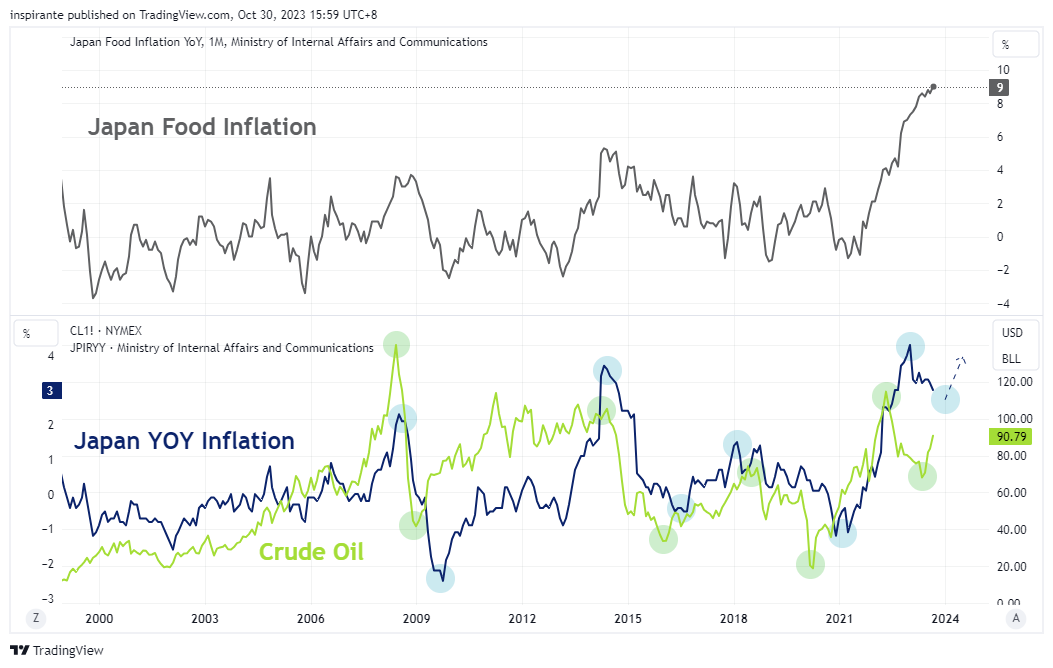

While we acknowledge that BoJ focuses on core inflation excluding food and energy. Japan's food inflation remains at multi-decade highs. Additionally, fluctuating oil prices this quarter might lead to heightened inflation, given Japan's role as a significant energy importer. The correlation between oil and the CPI is evident, with CPI trends following oil price changes.

Two lines in the sand become tested as:

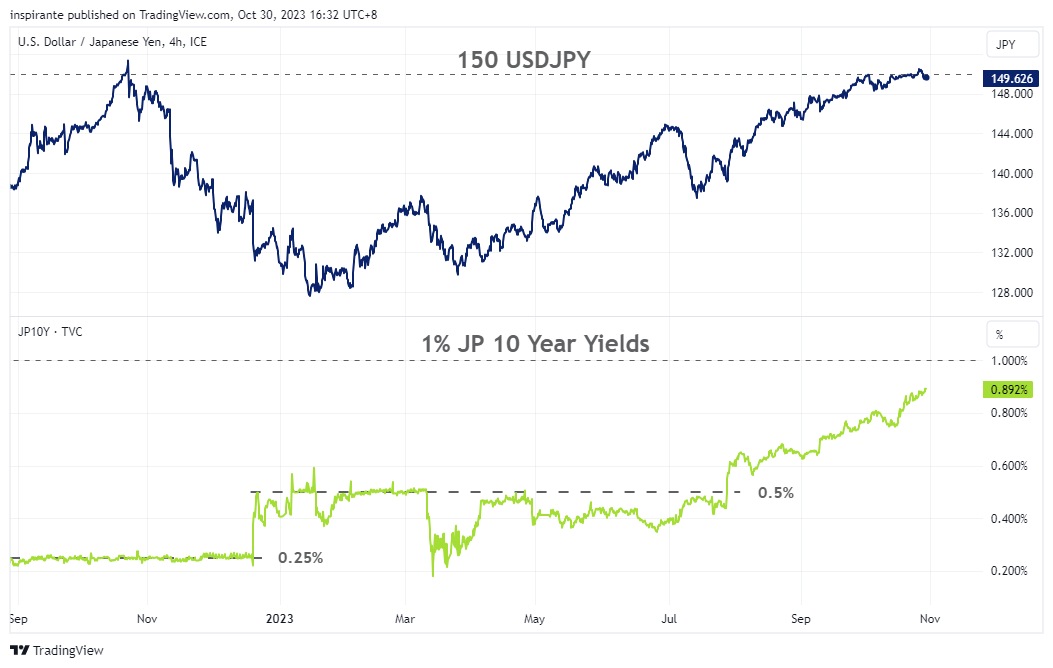

The USDJPY is inching closer to the significant 150 level—a threshold where the Ministry of Finance (MOF) intervened last October.

Japanese 10-year yields approach the 1% cap set by the BoJ in July.

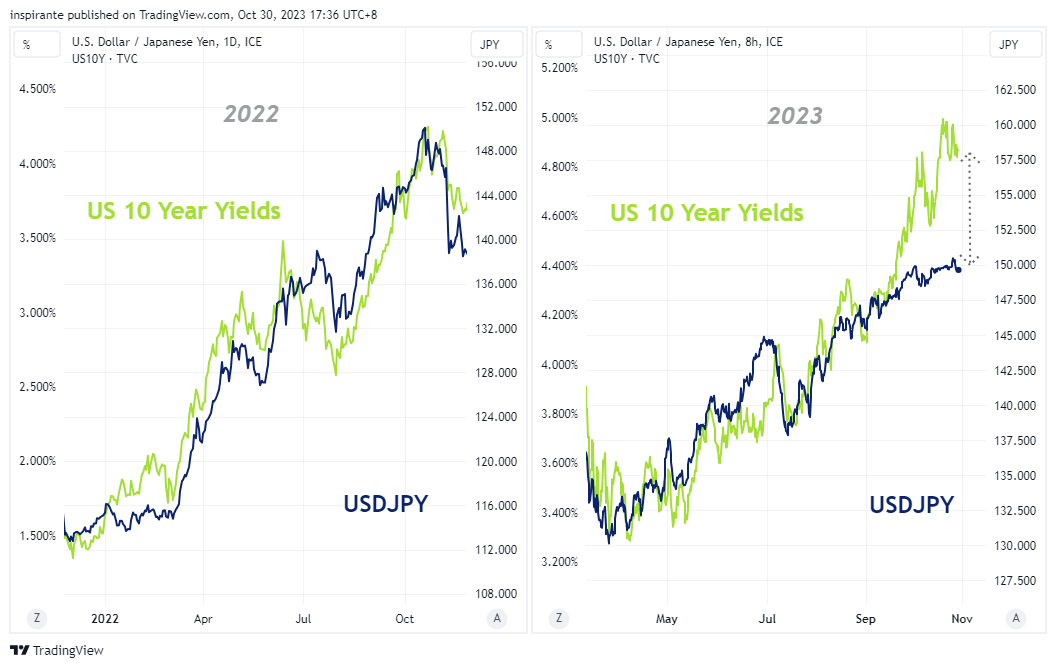

The relationship between US 10-year yields and the USDJPY currency has started to show divergence. This pattern mirrors the May–November 2022 period, which similarly illustrated a close relationship until MOF intervention.

What’s inside our playbook?

With the Bank of Japan meeting this week, Japan's monetary policy warrants attention, especially as it contrasts with its global counterparts.

Japan's long-term disinflationary trend has roots in unique factors like an aging population, consumer saving habits, and producers' reluctance to increase prices. Such challenges have necessitated unconventional central bank measures, including negative interest rates, yield curve control, and a sustained easing policy.

Two significant lines in the sand are now blurred:

The USDJPY's proximity to the 150 level. Almost exactly a year ago, in October 2022, the MOF's successful intervention caused a nearly 15% drop in the USDJPY over three months.

Japan's 10-year yields nearing their 1% cap. Since 2022, every time the yields approach the threshold, the BoJ adjusts its stance, either by raising the yield cap or modifying the yield curve control's definition.

Japan’s current inflation surge has inflation levels now above its central bank target and long-term average. Whilst this seems to have broken the disinflationary trend, we find cause for concern as food inflation remains incessantly high, and recent inflation prints come in higher than estimates. Adding to all that, the fact that Japan is one of the largest energy importers, a weakening currency only drives the inflation problem further. With oil turning higher this quarter over geopolitical events, the risk of a double whammy of higher energy prices and weaker currency could doubly amplify the toll of energy inflation in Japan.

Such dynamics shift attention towards potential monetary interventions aimed at curbing inflation growth. One avenue could be currency intervention, a strategy the MOF has employed previously. Past interventions around the 150 USDJPY threshold prove that the BoJ and MOF are watchful and worried about currency weakening.

Another avenue could be via a shift in interest rates. The recent surge in yields in the US has resulted in the further widening of the yield differential between the US and Japan, feeding into the problem of weakening currency. Again, on this front, BoJ governor Ueda has proven that the yield caps have room to move via previous policy tweaks in previous meetings.

Taking inflation, interest rates, and currency into account, the BoJ might consider increasing the yield cap as a countermeasure to currency frailty. Alternatively, the MOF might opt for intervention to resist yen devaluation trends, a tactic they've demonstrated in the past. Whichever route is chosen, if any, the market could witness swift reactions, potentially leading to more extensive risk events.

Executing the plays

A hypothetical investor can consider the following two trades1:

Case Study 1: Short SGX USDJPY (Standard) FX Futures (UY)

We would consider going short the USDJPY using a short position on the SGX USDJPY (Standard) FX Futures (UY) on the potential of a Yen intervention or policy tweak. Keeping in mind the volatile nature of the currency move in the event of this catalyst playing out. We can express a short position at the current level of 149.70, a tight stop at 152 and take profit of 144 will give a reasonable risk reward. Each 0.005 move in the UY contract is for 500 Yen.

Case Study 2: Short SGX 10-Year Mini Japanese Government Bond Futures (JB)

We would consider taking a short position on the SGX 10-Year Mini Japanese Government Bond Futures (JB) to express the view that interest rates in Japan might go higher. As Yields and price are inversely related, a short position on the Futures which is quoted as price, is translated to a view on higher yields. A short position at the current level of 144.22, stop at 145 and take profit at 142.2 will give us a reasonable risk to reward. Each 0.01 move is equal to 1000 Yen.

Original Link: https://www.sgx.com/research-education/market-updates/20231030-derivatives-traders-playbook-two-lines-sand

Examples cited above are for illustration only and shall not be construed as investment recommendations or advice. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.