What’s next after Trump trades?

Written on 2024-12-01, first published on 2024-12-03

Markets in focus

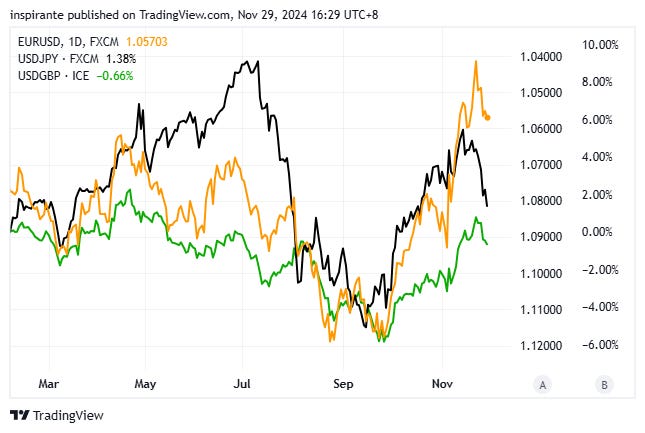

Leading up to the U.S. election, the U.S. Dollar has strengthened significantly against other major currencies like the EUR, JPY, and GBP.

Crude oil prices have been consolidating within the peak of a multi-year descending triangle pattern. A breakout below the support level could signal further downside potential.

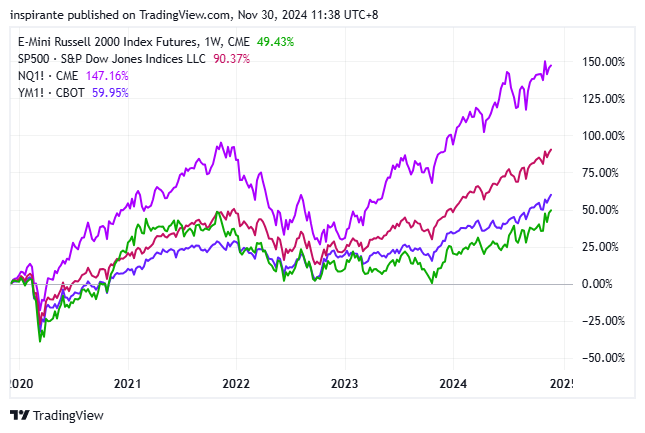

For the past 5 years, large-cap equities have consistently outperformed their small-cap counterparts. This outperformance is further amplified by the recent AI-driven rally.

In 2020 at the peak of the dot-com bubble there was a dramatic capital rotation from large-cap equities to small-cap. With new drivers now emerging from the US election result, this could signal the beginning of the reversal.

Our market views

The euphoria surrounding the “Trump trades” appears to have waned just weeks after completion of the U.S. presidential election. Initially, these trades dominated the investment landscape, driving U.S. stock markets to record highs, pushing Treasury yields upward, and strengthening the dollar amid expectations of tax cuts, increased government spending, and tariffs. Among these dynamics, two standout themes have emerged: a bearish outlook for crude oil markets and the rotation from large cap to small cap equities.

Trump’s pro-fossil fuel stance has undeniably bolstered investor confidence in the crude oil market. His emphasis on domestic energy production, coupled with expectations of deregulation and tax incentives for oil producers, suggests a supportive policy environment for the industry. However, this optimism is tempered by structural challenges in the market, notably oversupply and weak demand. While OPEC+ is anticipated to delay its planned output increases, U.S. crude oil production hit a record high in October, adding to the supply glut. Even the prospect of reinstating stringent sanctions on Iranian oil is unlikely to offset the oversupply. Additionally, geopolitical risks that typically support oil prices have eased, with the recent ceasefire between Israel and Hezbollah diminishing tensions in the Middle East.

Compounding these challenges, President-elect Trump announced last Monday new tariffs targeting the top three sources of U.S. imports: an additional 10% tariff on goods from China and 25% on products from Mexico and Canada. Although these tariffs are politically tied to issues like curbing illegal immigration and drug trafficking, their economic impact is undeniable. Even if the tariffs are not implemented, the mere threat of trade restrictions is likely to stifle global trade, eroding confidence in global economic activity. Against the backdrop of waning demand from China, these developments cast further doubt on the outlook for crude oil. As a USD-denominated commodity, crude oil prices also face downward pressure from the strengthening dollar.

Since the start of 2024, we have explored the potential for a rotation from large-cap to small-cap equities. This shift comes after years of consistent large-cap outperformance, amplified recently by the AI-driven rally. With Trump’s emphasis on “America First” policies, small-cap companies are now better positioned to benefit compared to their larger-cap counterparts. Key drivers of this shift include tax reforms, particularly corporate tax cuts, which are expected to provide significant relief to small-cap firms; many of which face higher effective tax rates than large multinationals. Additionally, infrastructure spending, a cornerstone of Trump’s agenda, is set to benefit industrial and materials sectors that are heavily represented within the Russell 2000.

Deregulatory measures, especially in sectors like financials and energy, could further ease compliance burdens and unlock growth opportunities for smaller businesses. Unlike large multinationals that derive substantial revenue from global markets, small-cap firms are more insulated from disruptions in global trade, such as those caused by tariffs or geopolitical tensions.

While a stronger dollar and higher interest rates are traditionally headwinds for small-cap companies, the anticipated fiscal stimulus and deregulation under Trump’s administration could outweigh these challenges. Moreover, Trump’s preference for a low-interest-rate environment may prompt the Federal Reserve to ease rates more aggressively, providing additional support for the small-cap segment. Taken together, these pro-growth, domestically focused policies, alongside the relative underperformance of small caps over the past five years, make a compelling case for a dramatic capital rotation from large caps to small caps in the months ahead. A spread trade, such as long Russell 2000 and short Nasdaq, allows the capitalization on the expected relative outperformance of small caps over large caps while mitigating broader market risks. By offsetting exposure to large-cap declines with small-cap gains, this strategy provides a balanced way to benefit from the capital rotation while reducing vulnerability to factors that could affect equities as a whole.

How do we express our views?

We consider expressing our views via the following hypothetical trades1:

Case study 1: Short Crude Oil Futures

We would consider taking a short position in the Micro Crude Oil futures (MCLH5) at the current price of 67.65, with a stop-loss above 74.00, a hypothetical maximum loss of 74.00 – 67.65 = 6.35 points. Looking at Figure 2, if crude oil prices break below the support level, it has the potential to revert further down to the key support level at 43.00, resulting in 67.65 – 43.00 = 24.65 points. Each Micro crude oil futures contract is 1/10 of the standard WTI crude oil contract size, and thus represents 100 barrels, and each point move is 100 USD. E-mini crude oil futures contract is also available at ½ of the standard contract size.

Case study 2: Short Nasdaq / Russell 2000 ratio spread

We would consider taking a short position in the Nasdaq/ Russell 2000 Index ratio by selling two Micro E-mini Nasdaq 100 index future (MNQZ4) at the current level of 20,991, and buying seven Micro E-mini Russell 2000 index future (M2KZ4) at the current level of 2,447, with the ratio at 20,991/ 2,447 = 8.58. We would place the stop-loss above 10.00 for a maximum potential loss of 10.00 – 8.58 = 1.42 points. Each point move in the Micro E-mini Nasdaq 100 futures contract is 2 USD, and each point move in the Micro E-mini Russell 2000 index futures contract is 5 USD. Both legs have similar notional values

- Nasdaq leg: 20,991 x 2 x 2 = 83964 USD

- Russell leg: 2,447 x 5 x 7 = 85645 USD

We can look at two hypothetical scenarios to understand the approximate dollar amount of a 0.1 point move in the ratio.

Scenario 1: Assuming the Nasdaq 100 index stays unchanged, and the Russell 2000 index rallies to 2,475, the ratio becomes 20,991/2,475 = 8.48. The overall profit, which comes from the Russell position in this case is (2,475-2,447) x 5 x 7 = 980 USD.

Scenario 2: Assuming the Russell 2000 index stays unchanged, and the Nasdaq 100 index rallies to 21,240, the ratio becomes 21,240/ 2,447 = 8.68. The overall loss, which only comes from the Nasdaq position in this case is (20991-21240) x 2 x 2 = -996 USD.

In Scenario 1, the ratio drops by 0.1 points, yielding a profit of 980 USD from the long Russell 2000 position. In Scenario 2, the ratio rises by 0.1 points, yielding a loss of 996 USD from the short Nasdaq position. There is margin offset for Nasdaq/ Russell 2000 index ratio spreads.

Original link here.

EXAMPLES CITED ABOVE ARE FOR ILLUSTRATION ONLY AND SHALL NOT BE CONSTRUED AS INVESTMENT RECOMMENDATIONS OR ADVICE. THEY SERVE AS AN INTEGRAL PART OF A CASE STUDY TO DEMONSTRATE FUNDAMENTAL CONCEPTS IN RISK MANAGEMENT UNDER GIVEN MARKET SCENARIOS. PLEASE REFER TO FULL DISCLAIMERS AT THE END OF THE COMMENTARY.

| A guest post by

|